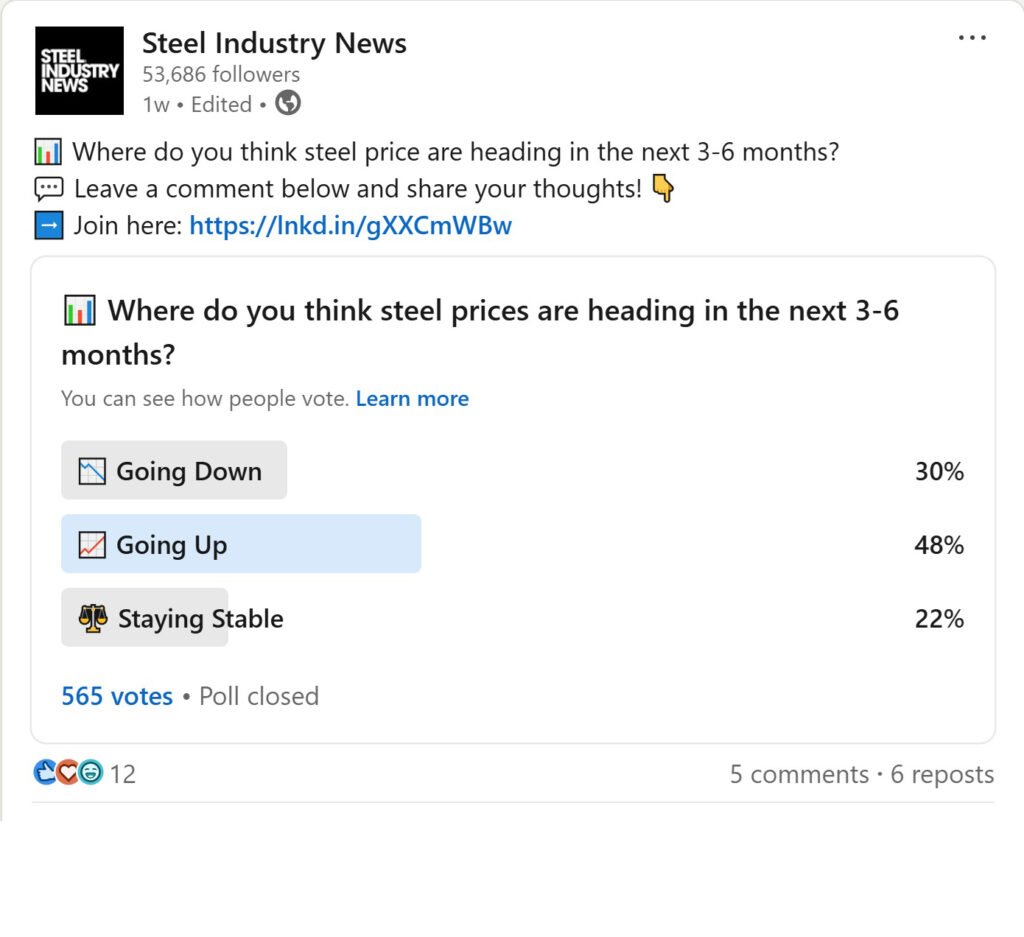

Steel pricing remains one of the most debated topics in the industrial sector, and the recent Steel Industry News 1 week Community Poll on LinkedIn brought this debate to the forefront. There was a total of 565 responses to the poll. With 168 votes for “Going Down,” 270 for “Going Up,” and 127 for “Staying the Same,” the poll captured a broad cross-section of industry sentiment about where steel prices are headed over the next 3–6 months. But what’s driving these opinions? This article dives deep into the survey responses, explores the reasoning behind each perspective, and connects these views to current market realities and data.

Steel Pricing Poll Results: A Snapshot of Industry Sentiment

The poll results reflect a divided market:

- 47% (270 votes): Steel prices will go up

- 29% (168 votes): Steel prices will go down

- 22% (127 votes): Steel prices will stay the same

This split highlights the uncertainty and complexity of the steel market in 2025. Let’s break down the reasoning and context behind each group’s outlook.

Why Do Many Expect Steel Prices to Rise?

A plurality of respondents believe steel prices are set to increase. This view is supported by several market dynamics and echoed in the poll’s comment section.

Key Factors Driving Bullish Sentiment

- Rising Raw Material Costs:

As one respondent, Brunello, noted, “it seems paradoxical, but even if the steel mills are producing less, the price is going up due to the increase of the energy costs … this is my personal opinion.” This reflects a widespread industry reality: higher energy and input costs are being passed through to steel buyers, regardless of demand softness. - Supply Constraints and Tariffs:

The reintroduction of tariffs and reduced import competition have given domestic mills more market power. Mills are able to raise prices and justify these increases as necessary to cover higher costs and fund new investments. This is especially true in the U.S., where tariffs are expected to keep prices elevated throughout 2025. - Strong Scrap Market:

The ferrous scrap market has seen three consecutive months of price increases, with Chicago’s prime scrap grades up 25% since the start of the year6. This tightness in raw materials is supporting higher finished steel prices, particularly as new electric arc furnace (EAF) capacity comes online and competes for limited scrap supply. - Infrastructure and Public Spending:

Ongoing infrastructure investments, such as those driven by the U.S. Infrastructure Investment and Jobs Act, are fueling optimism. As SDI CEO Mark Millet stated, “The continued onshoring of manufacturing businesses, combined with the expectation of significant fixed asset investment to be derived from public funding… will competitively position the domestic steel industry”. This view is reflected in the bullish responses anticipating a demand boost from public projects.

Case Study: U.S. Mills and Tariff Effects

| Factor | Impact on Pricing |

|---|---|

| Tariffs on Imports | Reduces competition, allows mills to raise prices |

| Raw Material Inflation | Higher costs passed to buyers |

| Infrastructure Spending | Sustains demand, supports higher prices |

Why Are Some Predicting a Price Drop?

Despite strong arguments for rising prices, a significant portion of respondents believe prices are heading downward. This view is rooted in concerns about demand and macroeconomic uncertainty.

Key Factors Behind Bearish Sentiment

- Decreasing Demand:

As Tamás Prokaj commented, “With decreasing demand, I would be particularly interested in this answer too.” This skepticism is grounded in real data: key steel-consuming sectors like automotive and agricultural equipment are facing challenges, with automakers cutting production and the agricultural sector seeing weaker equipment demand. - Global Economic Headwinds:

Forecasts from S&P Global and Market Consulting Intelligence suggest that steel prices could decline in 2025, with expectations of a trough around mid- to late-year. These projections are based on slowing global growth, especially in China’s property sector and in U.S. manufacturing. - Capacity Overhang:

While mills have curtailed some production, global capacity remains high. If demand fails to rebound as expected, oversupply could pressure prices lower, especially as new EAF capacity ramps up.

Market Data: Demand vs. Supply

| Indicator | Recent Trend |

|---|---|

| U.S. Automotive Production | Down 12% in March |

| Agricultural Equipment Demand | Weakening |

| Global Steel Demand (2025) | Up 1.2% (modest) |

| New EAF Capacity (U.S.) | +2.4 million tons |

The Middle Ground: Why Some Expect Stability

A notable minority expects prices to remain stable. This perspective is often grounded in the belief that the market is reaching a new equilibrium.

Key Arguments for Stable Prices

- Offsetting Forces:

Respondents in this camp see rising costs being balanced by soft demand, resulting in a “higher for longer” plateau rather than sharp moves in either direction. - Market Power and Volatility:

Mills may test the market’s tolerance for higher prices, but without extreme shortages or surpluses, prices could stabilize at a new, higher baseline5. - Sectoral Balancing:

While construction and infrastructure remain strong, weakness in automotive and agriculture could keep overall demand flat, supporting a sideways pricing trend.

Survey Comments: Industry Voices on Steel Pricing

The poll’s comment section provides valuable qualitative insight into the numbers.

Daniel:

“For the people that voted the price is headed upward, what is your reasoning?”

Tamás:

“With decreasing demand, I would be particularly interested in this answer too.”

Brunello:

“It seems paradoxical, but even if the steel mills are producing less, the price is going up due to the increase of the energy costs … this is my personal opinion.”

These LinkedIn poll comments highlight the core debate: can higher costs and supply constraints outweigh weaker demand, or will economic headwinds force prices down?

Market Data and Poll Sentiment: Are They Aligned?

Recent market data supports both sides of the debate:

- Prices Are Trending Higher:

Steel prices have been rising due to increased demand in select sectors and higher raw material costs. U.S. hot-rolled coil prices, for example, recently surged before stabilizing at elevated levels. - Volatility Remains High:

The market is experiencing increased price volatility as it adjusts to tariffs, supply chain shifts, and global uncertainties. - No Extreme Shortages:

Despite higher prices, the market is not experiencing the kind of shortages seen in the 2020–2021 bull market. Mills have capacity to spare, and future gains may be capped if demand doesn’t rebound strongly.

Conclusion: The Steel Pricing Poll as a Market Barometer

The Steel Industry News Community Poll provides a real-time snapshot of industry thinking-and reveals just how complex and nuanced the steel market is in 2025. The largest group expects prices to rise, citing tariffs, higher costs, and infrastructure demand. A substantial minority sees prices falling, pointing to weak demand and macroeconomic risks. Others expect stability as the market finds a new balance.

Ultimately, the poll’s diversity of opinion mirrors the broader market’s uncertainty. For buyers, sellers, and analysts, this means closely monitoring both macro trends and sector-specific developments will be crucial for navigating the months ahead.

Check out some of our other recent articles on the subject:

- Tariff Update May 2026: Section 232 Restructured, IEEPA Struck Down

- CSP HRC Hits $1,095 as Construction Bends

- [New eBook] Steel Buyers Decision Framework

- HRC CSP Climbs Again | Is the Ceiling Coming Near?

- Steel Procurement Framework: Buy, Wait, or Hedge?

Be sure to subscribe to the Steel Industry Email Newsletter to get the latest steel news delivered straight to your inbox!

Whether you choose our free subscription or upgrade to the premium version, your support helps us cover operational costs and continue providing the latest Steel Industry News at no charge.

By subscribing you agree to our Terms of Use, our Privacy Policy and our Information collection notice