Key Takeaways

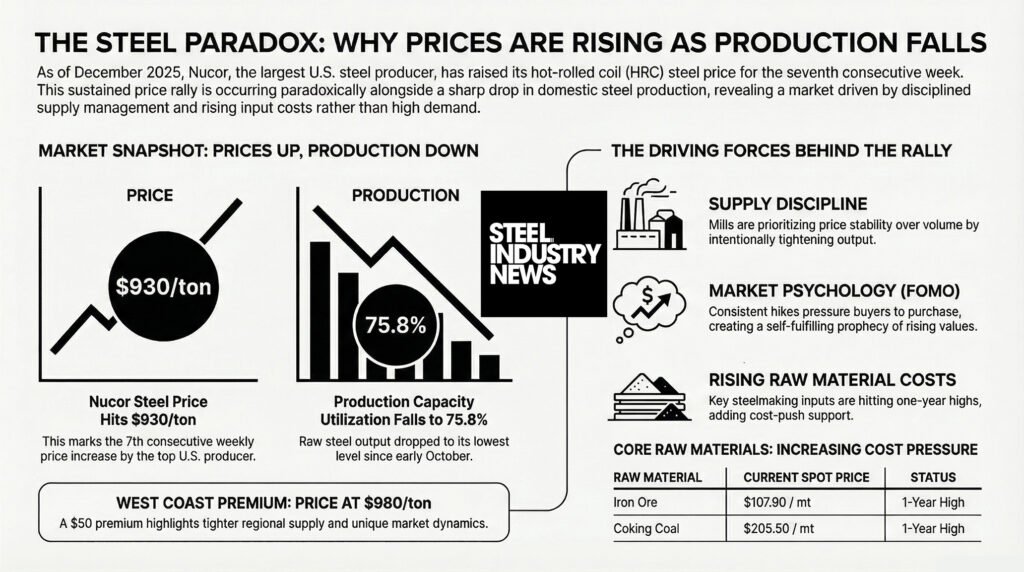

✅ Nucor Extends Price Rally: For the seventh consecutive week, Nucor has raised its Consumer Spot Price (CSP) for hot-rolled coil (HRC), effectively setting the new benchmark at $930 per ton for most regions and $980 per ton for California Steel Industries (CSI).

✅ Supply Tightening Drives Momentum: Despite a sharp drop in domestic raw steel production to 1.736 million tons and a utilization rate of 75.8%-the lowest since early October-prices continue to climb, signaling strict supply discipline from U.S. mills.

✅ Regional Variances Widen: While the overall market strengthens, the West Coast premium remains distinct with CSI pricing $50/ton higher, while the Southern region experienced the most significant production decline during the Thanksgiving holiday week.

Analyzing the 7th Consecutive HRC Increase

The U.S. steel market is witnessing a decisive shift in momentum as it enters the final weeks of 2025. For the seventh week in a row, Nucor Corporation-the largest steel producer in the United States-has announced a price increase, solidifying a bullish trend that has taken hold since late October.

Effective immediately for the week of December 8, 2025, Nucor’s Consumer Spot Price (CSP) for Hot Rolled Coil (HRC) has risen to $930 per short ton for the majority of its producing mills. This marks a $10 per ton increase over the previous week.

This sustained rally is occurring against a backdrop of tightening supply and lowered production rates, creating a complex environment for buyers in the construction, automotive, and manufacturing sectors. As we approach 2026, the market is signaling that the era of aggressive destocking may be over, replaced by a renewed focus on price stability and mill discipline.

The Anatomy of the Hike: Understanding the $930 Benchmark

Nucor’s pricing strategy, transparently communicated through its weekly CSP mechanism, serves as a bellwether for the domestic industry. The current increase to $930 per ton represents not just a single data point, but a continued effort to recover margins after the softness seen in the third quarter of 2025.

The CSI Premium

A critical distinction in this week’s announcement is the pricing divergence for California Steel Industries (CSI). While the general CSP is set at $930, the base price for CSI is set at $980 per ton.

This $50 premium highlights the unique dynamics of the West Coast steel market. CSI, a joint venture involving Nucor, operates in a region often geographically isolated from the heavy production centers of the Midwest and South. The West Coast typically faces higher logistics costs for domestic transport and different import parity levels compared to the Gulf or East Coast. For buyers in the Western region, this signal reinforces that regional availability is tighter, and the cost of procurement will remain elevated compared to the national average.

Production Dynamics: The Supply Side Story

While prices are rising, physical steel output has taken a notable dip. According to the latest available data, domestic raw steel production dropped sharply during the Thanksgiving holiday week, a traditional period for maintenance and reduced shifts.

Key Production Statistics:

- Total Output: U.S. mills produced an estimated 1,736,000 tons of raw steel.

- Change: This is down from 1,761,000 tons the previous week.

- Utilization Rate: The capacity utilization rate fell to 75.8%, down from 76.9%.

This utilization rate of 75.8% is significant. Historically, mills achieve strong pricing power when utilization exceeds 80%. However, the current scenario-rising prices amidst sub-80% utilization-suggests a different driver: Supply Discipline.

Rather than flooding the market to chase volume, mills appear to be carefully managing output to match reduced holiday demand. By keeping supply tight, they prevent inventory bloat, thereby supporting the $10/ton price hike even as physical shipments temporarily slow down. This is the lowest weekly output and utilization rate recorded since the first week of October, underlining the severity of the Thanksgiving curtailments.

Regional Analysis: The Southern Drop

The production decline was not uniform across the United States. Data indicates that production slipped in four of the five major steel-producing regions, with the Southern region experiencing the largest decrease in total tonnage.

The South is a powerhouse for electric arc furnace (EAF) production, a method heavily reliant on scrap metal and electricity. A sharp drop here could be attributed to several factors:

- Energy Management: Mills may have idled furnaces to avoid peak electricity pricing windows or to perform end-of-year maintenance.

- Inventory Control: With the fiscal year-end approaching for many companies, Southern mills might be reducing work-in-progress inventory to clean up balance sheets.

For buyers sourcing from Southern mills, this tightening of local supply could lead to extended lead times in January 2026, as mills ramp back up to meet the new $930 price point.

Market Implications: Cost-Push or Demand-Pull?

Is the current Nucor steel price rally driven by roaring demand or rising costs? The answer appears to be a mix of cost recovery and psychological momentum.

The Psychology of the “Seventh Hike”

When a mill raises prices once, the market may ignore it. When they raise it seven weeks in a row, buyers take notice. This consistency creates a “Fear of Missing Out” (FOMO) dynamic. Service centers and end-users who were waiting for the “bottom” in October are now realizing they missed the low point.

This psychology forces buyers off the sidelines. To avoid paying $950 or $1,000 per ton in January, procurement managers are booking tons at $930 now. This wave of buying activity validates the mill’s asking price, creating a self-fulfilling prophecy of rising values.

The Role of Scrap and Raw Materials

While specific scrap settlement numbers fluctuate monthly, the correlation remains strong. If prime scrap inputs (busheling) remain expensive or scarce, EAF mills like Nucor cannot afford to lower HRC prices. The $10/ton hike likely reflects a defensive move to maintain spreads between raw material costs and finished steel selling prices.

Spot iron ore prices have risen for the second consecutive week, reaching their highest level since July 2024 at $107.90 per metric ton, up from $104.80/mt the previous week, a 2.96% week-over-week increase. This one-year high is being driven by improving Chinese demand ahead of key year-end government meetings, combined with tighter port inventories that are constraining available supply.

At the same time, coking coal pricing has continued its upward momentum, also climbing to a one-year high. Spot coking coal ended the week at $205.50/mt, up from $199.00/mt a week earlier, marking the highest level since November 2024. Chinese government pressure on curbing overproduction among coal miners is expected to persist into year-end, effectively limiting supply and supporting elevated coal prices.

Key takeaway: Rising costs for core steelmaking inputs – iron ore and coking coal – are reinforcing mill efforts to raise and hold higher finished steel prices, providing additional cost-push support to Nucor’s latest HRC price moves.

Conclusion: Looking Toward 2026

The week of December 8, 2025, serves as a pivot point for the steel industry. Nucor’s move to push HRC prices to $930/ton- and $980/ton at CSI – demonstrates a confident stance on market stability.

The data presents a clear narrative: U.S. mills are prioritizing price integrity over volume. By allowing utilization to drop to 75.8% while simultaneously raising prices, they are sending a message that cheap steel is not available, regardless of demand levels.

For steel buyers, the window to negotiate significant discounts is closing. With the seventh consecutive hike now effective, the floor for Q1 2026 pricing is being set higher than many analysts predicted just two months ago. The key question for the remainder of December will be whether demand can support these levels once the holiday season concludes and full production resumes.

Reflective Question for Buyers: With utilization rates low and prices high, is your inventory strategy prepared for a potential supply squeeze in January if demand rebounds faster than mill ramp-ups?

SOURCES

1. Nucor’s Six-Week Price Surge: What It Signals for the Steel Market

https://steelindustry.news/nucors-six-week-price-surge-what-it-signals-for-the-steel-market/

2. Nucor Consumer Spot Price (CSP) Official Page

https://www.nucor.com/weekly-spot-price

(This is the official landing page where Nucor posts the weekly announcements cited in the article).

3. American Iron and Steel Institute (AISI) – Weekly Raw Steel Production

https://www.steel.org/industry-data/weekly-raw-steel-production/

(The source for the utilization rate of 75.8% and production tonnage of 1.736k tons).

4. Nucor Introduces New Hot-Rolled Coil Spot Pricing

http://nucor.com/news-release/nucor-introduces-new-hot-rolled-coil-spot-pricing-122529

5. World Steel Dynamics – Nucor CSP Price Analysis

https://www.worldsteeldynamics.com/nucor-csp-price-flat-other-major-indexes-soften/

Disclaimer

The content provided in this article is for general informational purposes only and does not constitute financial, legal, or professional advice. Readers should seek consultation with qualified professionals before making any financial, investment, or legal decisions. We disclaim any liability for losses, damages, or adverse outcomes resulting from decisions made based on the information presented herein.

Check out our most recent articles below:

- HRC CSP Hits $1,080 | Input Costs Climb | Capacity at 80.4%

- Steel Forecasting 2026: The Old Model Fails, A New Framework

- HRC Climbs to $1,070, Manufacturing PMI Holds at 52.7, ISM Prices Hit 2022 Highs, Iran War Enters Month Three: What It Means for Steel Buyers

- How AI, Robotics, and Automation Are Reshaping the Steel Industry in 2026

- HRC CSP Up $10/ton: What Rising Steel Prices Mean for Buyers

📬 Enjoying this article? Do not miss the next one.

Subscribe below to the Steel Industry News email newsletter to get the latest updates delivered straight to your inbox, including comprehensive reporting on the steel industry, plus the latest podcast, video, ebooks, and industry insights, so you receive the most recent steel news reports in one easy-to-read format

Your all-access pass to steel industry insight – now 50% off for the holidays! (Through Jan 1st 2026) – Get The Steel Industry Newsletter’s best annual package for only $300/year – that’s a $300 savings off the regular $600 annual price. You’ll enjoy six months free compared to the monthly plan.

🔐 Annual Plan: Just $300/year – that’s 6 months free (a 50% discount compared to monthly)

By subscribing you agree to our Terms of Use, our Privacy Policy and our Information collection notice