✅ Key Takeaways

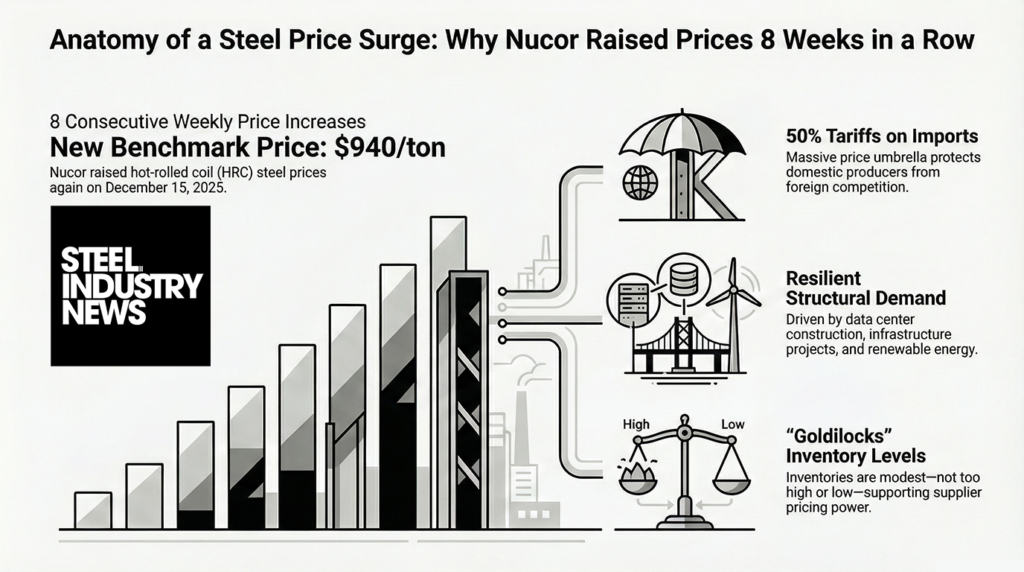

- ✅ Nucor announced its 8th consecutive weekly price increase on December 15, 2025, raising CSP HRC base prices by $10/ton to $940/ton, signaling strong market confidence and supply tightness in the US steel sector

- ✅ The pricing momentum reflects converging factors including solid demand from infrastructure projects, data center construction, tariff protection at 50%, and declining import competition, positioning Nucor for sustained pricing power in Q4 2025 and early 2026

- ✅ This pricing surge represents a strategic milestone for the steel industry, with implications for downstream manufacturers, construction companies, and distributors who must recalibrate pricing models and inventory strategies for 2026

Introduction: Nucor’s Unprecedented Pricing Momentum in the Steel Market

The steel industry rarely witnesses extended periods of consistent price appreciation, but Nucor Corporation’s decision to raise prices for the 8th consecutive week marks a remarkable inflection point in the market cycle. Effective immediately for the week of December 15, 2025, Nucor increased its cold-rolled coil (CSP) hot-rolled coil (HRC) base price by $10 per short ton, bringing the benchmark price to $940/ton across all producing mills, except California Steel Industries (CSI), where the CSP HRC base price reached $990/ton.

This sustained pricing momentum – with cumulative increases totaling approximately $80 per short ton over eight weeks – reflects a fundamental shift in steel market dynamics that has profound implications for manufacturers, construction companies, distributors, and investors across the North American economy. Understanding the drivers behind Nucor’s aggressive pricing strategy and the broader market conditions supporting these increases is essential for industry participants seeking to navigate the volatile steel landscape in 2025 and beyond.

The significance of this pricing surge extends beyond Nucor’s quarterly earnings expectations. It signals a period where tariff protection, modest inventory levels, and reduced import pressure have converged to create an environment where major steel producers can exercise pricing power. This article explores the multifaceted factors driving Nucor’s price increases, the competitive dynamics shaping the market, and the potential trajectory for steel prices heading into 2026.

Understanding Nucor’s Strategic Pricing Strategy in 2025

The Evolution of Nucor’s Pricing Power Through the Year

Nucor’s pricing trajectory throughout 2025 reveals the company’s strategic response to a dynamic and often unpredictable market environment. Earlier in the year, Nucor had established a CSP HRC base price of $760/ton in late January 2025, reflecting a more defensive posture during a period of industrial uncertainty. However, as market conditions evolved through the spring and summer, the company gradually began implementing price increases to capture improving demand and protect against rising production costs.

By August 2025, Nucor moved to reverse a price decline with a $10/ton increase to $875/ton, marking what the company described as “the first upturn in Nucor’s HR list price since the beginning of July.” This decision represented a strategic inflection point, signaling management’s confidence that the market had stabilized and that demand-supply dynamics had begun favoring producers over customers.

The momentum from August carried through autumn, with the company implementing consistent $5/ton increases in September and October 2025. By early November, Nucor’s CSP HRC price had climbed to $890/ton, setting the stage for the more aggressive pricing posture that would define Q4 2025. The progression from $890/ton to the current $940/ton represents an acceleration in pricing power, with Nucor shifting from cautious $5/ton weekly increases to more substantial $10/ton hikes.

Competitive Positioning: Nucor as a Market Leader

Nucor’s aggressive pricing strategy is underpinned by its position as one of North America’s largest and most efficient steel producers. The company operates multiple state-of-the-art mills using electric arc furnace (EAF) technology, which provides cost advantages over integrated steelmakers, particularly when scrap prices remain moderate relative to finished steel valuations. This cost structure gives Nucor the flexibility to maintain margins while competitors struggle during pricing downturns, and conversely, to capture premium margins during price upswings.

The company’s strategic focus on innovation and productivity – a cornerstone of its competitive strategy – has enabled Nucor to achieve industry-leading operational efficiency metrics. By investing consistently in technology upgrades and maintaining a lean, incentivized workforce structure, Nucor reduces its manufacturing costs per ton below those of most competitors. This cost leadership translates directly into pricing power: when other producers must raise prices to protect margins, Nucor’s lower cost base allows it to raise prices more aggressively while still maintaining acceptable return on capital metrics.

Moreover, Nucor’s market share gains across critical product segments underscore its competitive strength. In Q3 2025, the company achieved record rebar shipments and expanded market share in bar and structural products, particularly in high-growth sectors like data center infrastructure, renewable energy, and manufacturing expansion. These successes reflect Nucor’s strategic positioning in end-markets experiencing robust demand, which provides confidence in sustaining premium pricing.

Market Drivers Behind the 8-Week Price Increase Momentum

The Tariff Landscape: Structural Support for Domestic Pricing

One of the most consequential factors supporting Nucor’s pricing power is the elevated tariff structure protecting US steel producers from international competition. In June 2025, President Trump issued a proclamation that doubled Section 232 tariffs on steel imports from 25 percent to 50 percent for all countries except the United Kingdom, which remains subject to a 25 percent tariff. This dramatic increase in import barriers fundamentally altered the competitive landscape for US steelmakers.

The 50 percent tariff on imported steel effectively raises the delivered price of foreign competitors’ products by half, creating a massive price umbrella that protects domestic producers like Nucor. When Asian and European steelmakers attempt to export to North America, they must absorb tariff costs that make their products significantly more expensive than domestically produced alternatives. This dynamic allows Nucor to raise prices without fear that price-sensitive customers will shift to imported material – the tariff differential is simply too large to overcome.

For context, benchmark HRC steel traded at approximately $476 per metric ton FOB from China in August 2025. When adjusted for the 50 percent Section 232 tariff, ocean freight, and landing costs, this imported material would reach the US market at prices substantially above current Nucor levels. In practical terms, the tariff structure provides Nucor and other domestic producers with pricing power that would be impossible in an open, tariff-free market.

The tariff environment also contributes to supply discipline among domestic competitors. When import alternatives are effectively priced out of consideration due to tariffs, producers can coordinate on pricing with reduced fear of market share loss to foreign competitors. This dynamic – where tariffs create conditions for more stable, higher pricing – has been a defining feature of the 2025 steel market.

Demand Fundamentals: Infrastructure, Data Centers, and Reshoring

Despite macroeconomic headwinds affecting some sectors, steel demand has remained resilient in 2025, driven by several structural growth factors that show no signs of abating. The explosion in data center construction represents perhaps the most significant demand driver for steel in 2025 and extending into 2026. Major technology companies are aggressively expanding cloud computing infrastructure to support artificial intelligence workloads, requiring massive new facilities that demand substantial quantities of structural steel, reinforcing bar, and specialty products.

Data center construction creates remarkably steel-intensive demand profiles. Each facility requires structural steel frameworks, floor systems, roof systems, and specialized components for cooling infrastructure and power distribution systems. These facilities typically require hundreds or thousands of tons of steel per project, and the construction cycle for major data centers spans multiple years. The pipeline of announced data center projects extends well into 2026, providing steelmakers with multi-year demand visibility.

Beyond data centers, renewable energy expansion continues driving significant steel demand. Solar installation projects require mounting systems and support structures, typically manufactured from fabricated steel products. Wind energy infrastructure similarly demands large quantities of structural steel for tower fabrication and foundation systems. With renewable energy investment accelerating as part of broader energy transition initiatives, this demand stream shows structural growth potential rather than cyclical volatility.

US infrastructure spending also contributes meaningfully to steel demand. While the construction industry faced headwinds in 2025 due to tariff impacts and builder confidence challenges, infrastructure investment specifically – including bridge rehabilitation, water system upgrades, and transportation network improvements – provides a relatively stable demand foundation. Federal and state-level commitments to infrastructure modernization create multi-year demand visibility that supports producer confidence in maintaining elevated pricing.

Manufacturing reshoring represents an additional structural demand driver that was less prominent in previous years but is becoming increasingly important. Companies seeking to reduce supply chain concentration risk and benefit from proximity to North American markets have announced substantial capital investments in US manufacturing capacity. These investments require steel for facility construction, equipment fabrication, and production line installations. While some of this reshoring has been tempered by tariff impacts on imported components, the long-term structural trend toward reduced off-shore concentration remains intact.

Inventory Dynamics: The “Goldilocks” Supply Environment

The steel market operates most efficiently when inventory levels are neither excessively high nor dangerously low. In Q4 2025, inventory levels appear to have reached what market participants describe as “modest” – a sweet spot that supports pricing power without creating panic buying or speculative hoarding behaviors.

Service center inventories, which represent a key indicator of downstream supply conditions, remained at moderate levels through October 2025, with days of supply hovering around 2.3-2.6 months. This level is low enough to ensure that service centers and distributors cannot postpone purchasing decisions indefinitely, but not so tight as to create emergency conditions that might trigger panic buying behavior.

This inventory profile provides optimal conditions for a supplier like Nucor to exercise pricing power. When inventory is too high, buyers can delay purchases and wait for price relief. When inventory is dangerously low, the market can seize up, creating volatility that frightens producers into price cutting. But at current “modest” levels, buyers must maintain steady purchasing to support operations without excessive working capital deployment, while suppliers know that their products remain scarce enough to support premium pricing.

The modest inventory environment also reflects the fact that the US steel market has not experienced dramatic demand spikes that would require pre-emptive inventory building. Unlike some previous cycles where buyers frantically accumulated inventory ahead of anticipated price increases or supply constraints, the current environment reflects a more normalized, steady-state demand pattern. This reduces the speculative inventory accumulation that sometimes distorts pricing signals.

Production Capacity Utilization: Operating Near Optimal Levels

US steel industry production capability utilization rates reached 77.0 percent through mid-November 2025, representing solid operating levels that reflect brisk demand without indicating crisis shortages. This level of utilization is healthy from a profitability perspective – it’s high enough to support premium pricing, but not so high that it creates bottlenecks or forced delivery delays that might trigger customer defection.

At these utilization levels, Nucor and other producers operate their mills efficiently, spreading fixed costs across good volume while maintaining quality and delivery reliability. The absence of extreme capacity constraints means that producers have flexibility in production scheduling, which allows them to respond to specific customer requests without complete supply chain disruption.

The December holiday season typically brings seasonal softness to steel demand, as does the transition into January 2025. Some analysts anticipated that Nucor might moderate price increases during this seasonally weaker period. However, the company’s decision to implement a $10/ton increase for the week of December 15 suggests management confidence that underlying demand will remain sufficiently strong to support premium pricing despite seasonal headwinds.

Comparative Analysis: Nucor’s Pricing vs. Market Benchmarks

Spot Price Trajectory and Index Comparisons

Tracking Nucor’s official CSP prices alongside independent market indices reveals important nuances in the supplier-customer dynamic. According to market assessments from early December 2025, independent benchmark prices for HRC steel ranged from approximately $820-$900/ton FOB mills east of the Rockies, with spot prices averaging around $870-$880/ton depending on the specific market check date and specific product specifications.

Nucor’s official CSP prices typically establish benchmarks that exceed spot market assessments by $30-$60 per ton, reflecting several factors. First, Nucor’s list prices represent official producer pricing to customers with established commercial relationships, while spot prices often reflect transactional activity in the physical or futures markets where more spot or lower-volume sales occur. Second, Nucor’s published list prices may apply different terms and conditions than spot market transactions, including availability, lead times, and specification flexibility.

The spread between Nucor’s $940/ton official CSP and independent market benchmarks around $870/ton reflects the company’s ability to command a premium based on its market position, product quality, delivery reliability, and the switching costs that established customers face when considering alternatives. This premium indicates that Nucor’s pricing power extends beyond the commodity benchmark level that financial analysts typically reference.

West Coast CSI Pricing: Localized Market Dynamics

Nucor’s subsidiary California Steel Industries (CSI) serves West Coast markets where different supply-demand dynamics and transportation costs create somewhat different price levels than East Coast markets. For the week of December 15, CSI’s HRC base price reached $990/ton, representing a $50/ton premium to the general Nucor CSP price of $940/ton.

This price differential reflects the unique characteristics of West Coast steel markets, including higher transportation costs from Midwest and East Coast producers, CSI’s position as a significant West Coast supplier, and the greater concentrations of certain customer segments (aerospace, automotive, specialty manufacturers) that value CSI’s capabilities sufficiently to pay premium pricing. The larger CSI premium ($50/ton) relative to CSI’s typical regional premium (typically $40-$60/ton) suggests that West Coast supply conditions may be even tighter than national averages.

The Eight-Week Price Increase Cascade: Analyzing the Acceleration

Weekly Price Movement Patterns

Examining the specific pattern of Nucor’s eight consecutive weekly price increases reveals strategic pricing decisions and market confidence evolution. Through early November 2025, the company implemented consistent $5/ton weekly increases, reflecting a measured, confidence-building approach that avoided shocking customers with sudden large price jumps. However, beginning in late November, the company shifted to more aggressive $10/ton weekly increases, doubling the pace of pricing escalation.

This acceleration in the price increase pace serves multiple strategic functions:

- Demand Capture: By accelerating price increases, Nucor accelerates the realization of improved margins before demand potentially softens

- Sentiment Shifting: More aggressive pricing sends a powerful market signal that supply conditions are tightening and demand conditions are strengthening, influencing customer purchasing behavior

- Competitive Coordination: More visible, aggressive pricing announcements from market leader Nucor often trigger corresponding pricing actions from competitors, supporting industry-wide price improvement

- Peak Cycle Realization: Management may perceive that the current favorable market window is time-limited, driven by seasonal demand patterns or expectations of softening demand in early 2026

Implications for Downstream Industries and Market Participants

Automotive Sector Exposure and Cost Pressures

The automotive industry represents a significant consumer of flat-rolled steel products, including HRC, cold-rolled coil (CRC), and galvanized products. The cumulative price increases implemented by Nucor create substantial cost pressures for vehicle manufacturers and automotive component suppliers already facing margin compression from labor cost increases, capital investment requirements for electric vehicle transition, and competitive pricing pressures in a global automotive market.

Major automotive assemblers have some ability to pass through increased steel costs to consumers through new vehicle pricing, particularly for premium vehicles where consumers demonstrate less price sensitivity. However, competitive dynamics in mass-market segments limit pricing flexibility, particularly if competitors sourcing from non-US suppliers can maintain lower input costs through tariff optimization strategies.

Automotive component suppliers, who often operate on relatively thin margins and have limited pricing power with major OEM customers, face particularly acute challenges from elevated steel prices. These suppliers must absorb cost increases, improve productivity to offset them, or exit market segments where margin compression becomes untenable.

Construction Industry Effects and Project Profitability

Construction companies rely on stable input costs to estimate project budgets and lock in contractual pricing with building owners. Rapid, substantial steel price increases like those implemented by Nucor complicate the construction industry’s ability to forecast costs accurately and establish firm pricing with clients. This uncertainty often leads contractors to increase their contingency provisions or request price escalation clauses in construction contracts, ultimately raising costs to end-building owners.

The construction industry’s Q4 2025 performance remains mixed, with the overall sector expected to contract 2.7 percent in 2025 according to industry forecasts. While infrastructure spending has remained relatively resilient, commercial, industrial, and residential construction segments have faced headwinds from tariff impacts and financing cost challenges. In this environment, contractors have limited ability to absorb elevated steel costs without reducing project margins or requesting contract revisions.

Service Centers and Distributors: Working Capital and Inventory Challenges

Steel service centers and distributors face distinct challenges from the rapid price increase environment. When prices are rising, service centers must decide whether to replenish inventory at current elevated prices (protecting against potential further increases but tying up working capital) or reduce inventory levels (preserving cash but risking stockouts if demand remains robust).

Service center inventory position as of October 2025 showed modest levels that provide some insulation against rapid price increases, but don’t provide the buffer that service centers would ideally prefer during periods of price volatility. The extension of lead times to 3-5 weeks further constrains service centers’ flexibility, as they cannot quickly source alternative supply if customer demand exceeds inventory availability.

Distributors and service centers also face margin pressure. While they benefit from price increases when they hold inventory purchased at lower prices, the extension of lead times and the rapid pace of price escalation can work against their interests by creating customer dissatisfaction if they cannot deliver products at the prices customers anticipated, or by forcing them to hold inventory longer at lower prices.

Competitive Dynamics: How Other Steelmakers Respond

Industry-Wide Pricing Coordination

When Nucor, as one of the industry’s largest and most transparent producers, announces significant price increases, competitors typically follow suit within days or weeks. This pattern reflects both competitive necessity – competitors must match prices to maintain market share – and the fact that when one major producer signals that the market can support higher prices, others gain confidence that customers will accept equivalent pricing adjustments.

In the current environment, regional producers and specialty steelmakers have generally followed Nucor’s pricing leadership, implementing increases that align with but may not exactly match Nucor’s moves. This pricing coordination is entirely legal and reflects competitive market dynamics rather than collusive behavior, as each company maintains the right to adjust its pricing independently based on its specific cost structure and market position.

Integrated steelmakers (companies operating integrated blast furnaces and steelmaking operations) face different cost structures than Nucor’s EAF mills, and this impacts their pricing flexibility. However, the current environment of strong pricing generally benefits all industry participants, and integrated producers have also implemented price increases during this period.

Import Discipline and Foreign Producer Pricing

The 50 percent Section 232 tariff maintains discipline in import pricing, effectively preventing price undercutting by foreign producers that would otherwise force US producers to moderate their pricing. This tariff structure ensures that even if prices rise significantly in the US market, foreign producers cannot exploit the price differential by shipping additional volumes to North America, as the tariff would eliminate any arbitrage advantage.

This dynamic represents a fundamental departure from pre-2018 markets, where tariff-free trade allowed global price discovery to constrain pricing power for domestic producers. The tariff structure provides what economists term “insulation” from global price competition, allowing US producers to exercise pricing power that would be unsustainable in an open market.

Risks and Uncertainties Surrounding the Pricing Environment

Demand Normalization and Cyclical Softness Risks

Despite near-term pricing strength, the fundamental growth outlook for US steel demand remains relatively modest at approximately 1.8 percent annually through 2026. This growth rate implies that any significant further price increases would depend primarily on supply constraints rather than demand surges. If demand normalizes to levels consistent with long-term growth trends, pricing pressure could emerge relatively quickly.

Additionally, certain end-markets face specific headwinds despite overall demand resilience. The automotive sector is navigating EV transition costs and competitive pressures, construction activity faces tariff-related headwinds, and commercial real estate faces structural challenges from office space displacement due to remote work trends. If any of these segments experience sharper-than-expected demand deterioration, it could dampen overall steel demand more rapidly than current forecasts suggest.

Competitive Capacity Expansion and Supply Additions

The steel industry has announced at least $10-15 billion in new greenfield steel plant construction in 2025, with total capital spending on expansions and upgrades potentially reaching $20-25 billion. Much of this capacity is scheduled to come online in 2025-2027. When new capacity begins operating, it will increase industry supply, potentially applying downward pressure on prices unless demand grows proportionally.

The current favorable pricing environment has encouraged capacity additions from both integrated steelmakers and EAF producers. Once this capacity comes online and reaches normal operating rates, the supply-demand balance could shift from tight to balanced or even oversupplied, triggering margin compression. This transition could be relatively rapid once new facilities begin operating at scale.

Policy and Tariff Uncertainty

The tariff environment supporting current pricing is not guaranteed to persist indefinitely. Trade negotiations with key countries, legal challenges to tariff implementation, or changes in administration policies could potentially modify the tariff structure that currently supports domestic steel pricing. Even modest reductions in tariff levels could have significant impacts on pricing dynamics by reducing the insulation from global competition.

Additionally, the distinction between tariff protection and other trade policies (such as tariff rate quotas or country-specific arrangements) creates potential for disruption if policies shift. Uncertainty about policy stability itself can influence customer behavior, either encouraging pre-emptive purchasing if customers fear higher tariffs, or encouraging inventory reduction if customers fear lower tariffs that would reduce prices.

Currency and Input Cost Volatility

Steel producers’ costs are influenced by scrap metal prices, energy costs, labor expenses, and other inputs that fluctuate based on macroeconomic conditions. While current scrap costs remain at moderate levels relative to finished steel prices, significant scrap price increases could compress margins. Similarly, energy cost volatility directly impacts EAF producers’ profitability, as electricity represents a substantial cost component.

Currency fluctuations between the US dollar and other currencies can also impact import pricing and the competitiveness of exports, creating additional volatility in the pricing environment.

Strategic Takeaways: What the Eight-Week Price Increase Signals

Market Participant Guidance

For steel customers and downstream users, the key implication is that the pricing environment remains unfavorable in the near term, with further price increases possible before demand softens sufficiently to support price moderation. Companies should prioritize securing long-term supply contracts at fixed or capped prices where possible, and continue pursuing productivity improvements and operational efficiency to offset higher input costs.

For industry participants and competitors, Nucor’s aggressive pricing approach is likely to trigger continued pricing discipline across the industry, with competitors generally following suit with equivalent or similar increases. However, the rate of price increases may begin to moderate as supply and demand dynamics become better balanced and as customer resistance to further increases becomes more apparent.

Conclusion: Navigating the New Steel Price Reality

Nucor’s decision to raise prices for the eighth consecutive week, bringing the CSP HRC base price to $940/ton, represents a significant inflection point in the US steel market. This sustained pricing momentum reflects a convergence of supportive factors including elevated tariff protection, robust demand from infrastructure and data center construction, modest inventory levels, and strong production capacity utilization rates.

The recent price increases from Nucor carry substantial implications for downstream industries including automotive, construction, and manufacturing. While the pricing environment should eventually moderate as supply additions come online and demand normalizes to trend growth rates, near-term indicators suggest that pricing power may persist through early 2026.

For industry participants navigating this environment, success depends on recognizing that the current pricing environment is likely cyclical rather than structural. Customers should focus on securing favorable long-term supply arrangements and pursuing productivity improvements. Competitors should balance near-term margin capture with investments in operational excellence that provide competitive advantages beyond temporary pricing cycles. Investors should appreciate the strong earnings potential of the current environment while maintaining realistic expectations about its duration.

The broader steel industry continues to demonstrate its essential role in supporting US infrastructure, manufacturing, and economic growth. As Nucor and its competitors exercise pricing power, the challenge becomes ensuring that elevated steel costs do not undermine the investment in data centers, renewable energy, and infrastructure that depends on affordable, reliable steel supply. The balance between capturing pricing momentum and maintaining long-term customer relationships and market share will define steelmakers’ success in the years ahead.

SOURCES

worldsteel. (2025, October 23). worldsteel Short Range Outlook October 2025. Retrieved from https://worldsteel.org/media/press-releases/2025/worldsteel-short-range-outlook-october-2025/

Trading Economics. (2025, December 15). HRC Steel – Price – Chart – Historical Data – News. Retrieved from https://tradingeconomics.com/commodity/hrc-steel

Yahoo Finance. (2025, December 12). Why The Narrative Around Nucor Is Shifting As Analysts Lift Long-Term Price Targets. Retrieved from https://finance.yahoo.com/news/why-narrative-around-nucor-shifting-120916891.html

Investing.com. (2025, December 11). Nucor Corp stock hits 52-week high at 166.31 USD. Retrieved from https://www.investing.com/news/company-news/nucor-corp-stock-hits-52week-high-at-16631-usd-93CH-4403726

Discovery Alert. (2025, October 31). Gerdau Reports Strong US Steel Demand Growth in 4Q. Retrieved from https://discoveryalert.com.au/us-steel-recovery-market-dynamics-2025/

White & Case. (2025, June 12). Trump Administration Increases Steel and Aluminum Section 232 Tariffs to 50%. Retrieved from https://www.whitecase.com/insight-alert/trump-administration-increases-steel-and-aluminum-section-232-tariffs-50-and-narrows

BCG. (2025, June 10). June 2025: 50% US Tariffs Steel and Aluminum Impact. Retrieved from https://www.bcg.com/publications/2025/june-2025-update-impact-us-tariffs-50-percent-on-steel-aluminum

Industrial Sage. (2025, December 6). U.S. Manufacturing Production 2025: PMI, Steel & Reshoring. Retrieved from https://www.industrialsage.com/headlines-episode-13/

AISI. (2025, November 16). Industry Data – Weekly Raw Steel Production. Retrieved from https://www.steel.org/industry-data/

Yahoo Finance. (2025, December 1). US Construction Industry Report 2025. Retrieved from https://finance.yahoo.com/news/us-construction-industry-report-2025-091300148.html

Disclaimer

The content provided in this article is for general informational purposes only and does not constitute financial, legal, or professional advice. Readers should seek consultation with qualified professionals before making any financial, investment, or legal decisions. We disclaim any liability for losses, damages, or adverse outcomes resulting from decisions made based on the information presented herein.

Check out our most recent articles below:

- Steel Procurement Framework: Buy, Wait, or Hedge?

- HRC CSP Hits $1,080 | Input Costs Climb | Capacity at 80.4%

- Steel Forecasting 2026: The Old Model Fails, A New Framework

- HRC Climbs to $1,070, Manufacturing PMI Holds at 52.7, ISM Prices Hit 2022 Highs, Iran War Enters Month Three: What It Means for Steel Buyers

- How AI, Robotics, and Automation Are Reshaping the Steel Industry in 2026

📬 Enjoying this article? Do not miss the next one.

Subscribe below to the Steel Industry News email newsletter to get the latest updates delivered straight to your inbox, including comprehensive reporting on the steel industry, plus the latest podcast, video, ebooks, and industry insights, so you receive the most recent steel news reports in one easy-to-read format

Your all-access pass to steel industry insight – now 50% off for the holidays! (Through Jan 1st 2026) – Get The Steel Industry Newsletter’s best annual package for only $300/year – that’s a $300 savings off the regular $600 annual price. You’ll enjoy six months free compared to the monthly plan.

🔐 Annual Plan: Just $300/year – that’s 6 months free (a 50% discount compared to monthly)

By subscribing you agree to our Terms of Use, our Privacy Policy and our Information collection notice