✅ Key Takeaways

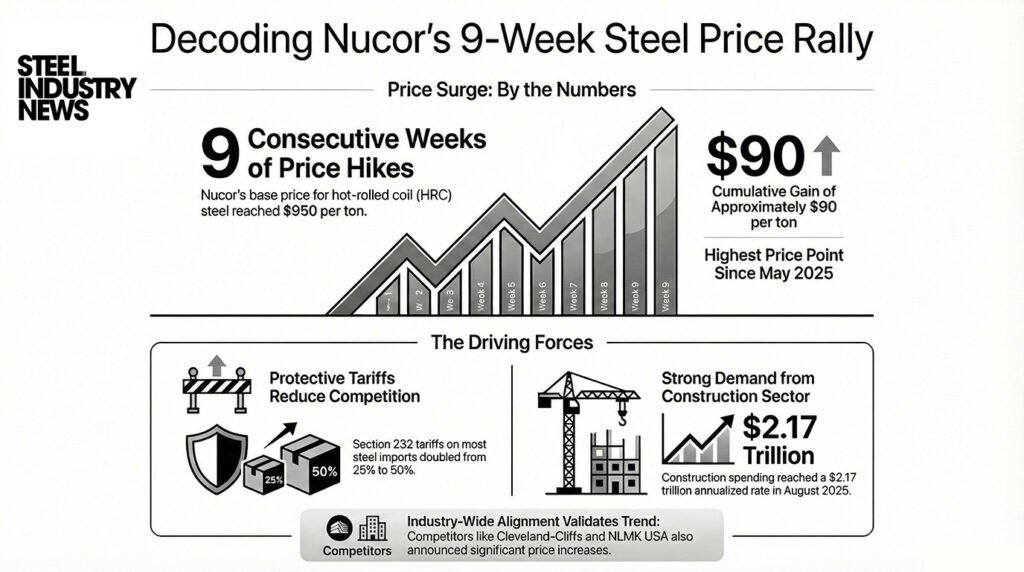

✅ Nucor’s 9-Week Rally: Nucor has raised hot-rolled coil prices by $10/ton for nine consecutive weeks, bringing the CSP HRC base price to $950/ton for most mills (and $1,000/ton for California Steel Industries), marking the highest pricing since May 2025.

✅ Tariff-Driven Strength: The 50% Section 232 steel tariffs implemented in June 2025 are supporting sustained domestic price increases by reducing import competition and creating supply discipline across North American steel mills.

✅ Infrastructure Demand Sustains Momentum: Construction spending reached $2.17 trillion annualized in August 2025, with federal infrastructure programs and nearshoring investments providing durable demand support for flat-rolled steel products.

Introduction: Understanding Nucor’s 9-Week Price Surge

Nucor Corporation has announced its ninth consecutive weekly price increase for hot-rolled coil (HRC), effective for the week of December 22, 2025. The company’s Consumer Spot Price (CSP) for HRC now stands at $950 per short ton for all producing mills, with the exception of its California Steel Industries (CSI) joint venture, where pricing reaches $1,000 per short ton – the highest levels observed since early May 2025. This sustained rally represents approximately $90 per ton in cumulative gains over nine weeks, reflecting a fundamental shift in supply-demand dynamics within the U.S. steel sector.

The significance of Nucor’s pricing actions extends far beyond internal mill economics. As North America’s largest steelmaker and a bellwether for industry conditions, Nucor’s pricing movements serve as a critical indicator of broader steel market health, downstream customer demand, and the lasting impact of tariff policies on domestic steel producers. Understanding what drives these price increases, how they compare to historical precedent, and what they signal about future market conditions is essential for supply chain professionals, investors, and industry observers seeking to navigate an increasingly complex and policy-driven steel market.

The Perfect Storm: What Triggered Nucor’s Nine-Week Rally

Section 232 Tariffs Reshape the Competitive Landscape

The foundation for Nucor’s sustained pricing power rests on the dramatic expansion of Section 232 steel and aluminum tariffs that took effect on June 4, 2025. The Trump administration doubled these tariffs from 25% to 50% on imports from nearly all countries, with limited exceptions including the United Kingdom at 25%. Boston Consulting Group estimated that these tariff increases alone would add approximately $50 billion in annual tariff costs across U.S. industries, effectively pricing out many foreign competitors from the domestic market.

This tariff regime fundamentally altered the economics of steel procurement in North America. Rather than face 50% duties on imported hot-rolled coil from Europe, Asia, or other regions, downstream customers – including automotive suppliers, construction fabricators, and industrial equipment manufacturers – have been compelled to source increasingly from domestic producers like Nucor, Cleveland-Cliffs, U.S. Steel, and NLMK USA. The tariff wall created a protective moat around U.S. steelmakers, enabling them to raise prices with considerably less competitive pressure than would exist in an open trade environment. This dynamic is not new to the steel industry, but the magnitude of the tariff increase and its broad application to derivative products amplified its impact significantly.

Furthermore, the June 2025 proclamation expanded the scope of tariffs beyond primary steel articles to include non-steel content in composite products, creating additional complexity and cost for importers and further supporting domestic pricing. The cumulative effect has been a sustained improvement in mill operating rates and order backlogs across the domestic industry, enabling producers to implement regular price increases with relatively short lead times (3-5 weeks) and stable customer commitments.

Construction Spending Provides Durable Demand Support

While tariffs create a supply-side advantage for domestic producers, sustained demand from downstream industries provides the essential pull-through mechanism that justifies repeated price increases. The U.S. construction sector, which accounts for the largest share of domestic steel demand, has demonstrated surprising resilience through 2025 despite macroeconomic headwinds and financing challenges. According to data released by the U.S. Census Bureau, total construction spending during August 2025 reached $2,169.5 billion on a seasonally adjusted annual rate basis, translating to a projected $2.23 trillion in total put-in-place construction spending for 2025 – a 3.3% increase from 2024 levels.

The composition of this demand is particularly supportive for hot-rolled coil and plate products. Infrastructure construction, the fastest-growing segment within the broader construction market, is projected to expand at nearly 8% CAGR through 2030, driven by federal spending programs authorized under the Infrastructure Investment and Jobs Act and additional capital allocation programs. These infrastructure projects – spanning highway construction, water systems, energy transmission, renewable energy installations, and broadband expansion – consume significant tonnages of structural steel, flat-rolled products, and specialty sections that drive demand to integrated mills like Nucor.

Institutional construction in healthcare, education, and government facilities is also expected to grow by 6.1% in 2025, further supporting steady steel consumption. While residential construction has faced headwinds from elevated mortgage rates and housing affordability challenges, nonresidential construction is projected to grow by 1.7% in 2025 and 2.0% in 2026, providing a floor under broader construction activity. This multi-sector support for construction spending translates directly into sustained order flow for primary steel producers and justifies their ability to raise prices sequentially without facing demand collapse.

Automotive Recovery: A Secondary But Important Driver

Although automotive production did not accelerate dramatically in 2025, it has stabilized at levels that support steady steel demand. U.S. light vehicle production is expected to reach approximately 10.45 million units in 2025, representing modest growth of 1.16% compared to 2024, according to AutoForecast Solutions. This modest but positive trajectory is significant in the context of 2024, when uncertainty around tariff policy and economic conditions had depressed capital allocation in automotive supply chains.

The automotive sector represents approximately 20-25% of overall steel demand in the United States, with particularly high penetration in galvanized and cold-rolled sheet products where automotive accounts for 40% of output. As dealer inventories have normalized to more sustainable levels (approximately 57 days of supply, close to the historical norm of 60-70 days), automakers have returned to steadier production schedules that support consistent mill utilization and ordering patterns. This stabilization in automotive demand, combined with improving infrastructure and institutional construction, creates a demand profile that allows Nucor to maintain discipline on pricing while preserving customer relationships and order flow.

Nucor’s Pricing Power: Historical Context and Market Implications

How the 9-Week Rally Compares to Historical Precedent

Nucor’s current nine-week rally of $10 per ton per week represents aggressive but not unprecedented pricing action. In historical context, this pace of increases is consistent with periods of tightening supply or rapidly improving demand fundamentals, though the current environment differs significantly from historical precedent in several important ways.

During the 2020-2021 recovery period, following the initial COVID-19 demand collapse, steelmakers implemented steep price increases as pandemic-related supply disruptions intersected with massive fiscal stimulus demand. However, those increases were often interrupted by periodic pullbacks as supply caught up or demand moderated. The current 2025 rally, by contrast, has maintained consistency week-after-week without interruption, suggesting underlying market tightness or strategic production discipline rather than reactive scrambling for order flow.

Earlier in 2025, Nucor demonstrated more cautious pricing. In January 2025, the company set an HRC base price of $760/mt ($760/short ton equivalent), and throughout the first quarter maintained relatively flat positioning as market uncertainty around tariff policies remained high. The company cut prices modestly in April 2025 by $5 per ton, the first reduction of the year, reflecting weak spring demand that materially disappointed end-users. This demonstrated that even with tariff protection, Nucor cannot indefinitely sustain price increases without underlying demand support – a critical distinction from a purely supply-constrained market.

The current rally differs fundamentally because it emerges against the backdrop of clarified tariff policy (the 50% rates are now fully implemented and show no signs of reversal), proven demand resilience (construction spending is running ahead of pre-tariff expectations), and demonstrated production discipline (competitive mills like Cleveland-Cliffs and NLMK USA have announced their own price increases, indicating industry-wide conviction). This alignment of favorable conditions – tariff protection, demand support, and collective producer discipline – provides a much more durable foundation for sustained pricing than typical cyclical upswings.

Competitive Dynamics: Are Other Steelmakers Following Suit?

One critical indicator of whether Nucor’s pricing reflects genuine market strength versus isolated market leadership is whether competitors are also implementing price increases. The evidence strongly suggests industry-wide pricing improvement. Cleveland-Cliffs, the second-largest domestic steelmaker, opened its May 2025 order book at $975 per ton, up from $900 per ton in April – a $75 per ton monthly increase that outpaced Nucor’s pace at the time. NLMK USA announced a $50 per ton price increase in late October 2025, following an earlier $50 per ton increase in late September, signaling its own assessment of improving market conditions.

This competitive pricing alignment is crucial because it indicates that Nucor’s price increases are not simply a function of aggressive sales tactics or market share defense, but rather reflect genuine limitations on supply availability or durable shifts in demand-supply balance that affect the entire industry. When multiple producers with different ownership structures, geographic footprints, and product mixes all converge on similar pricing trends, it suggests that macroeconomic and tariff drivers are overpowering company-specific factors. This competitive validation significantly increases confidence that the current price levels are sustainable rather than a temporary anomaly driven by temporary market mismatch or short-term supply constraints.

Industry Headwinds and Sustainability Concerns

Demand Uncertainty and End-User Caution

While the demand picture has improved, end-users remain cautious about accumulating expensive inventory. Steel World Review noted in November 2025 that “service centers reduce their activity toward the end of the calendar year, anticipating seasonal sales declines and being cautious about accumulating expensive inventories.” This seasonally typical behavior, combined with uncertainty about potential tariff policy changes in 2026, may limit the breadth and depth of buying interest in the coming months.

Additionally, while infrastructure spending has been robust, the flow of actual project starts and customer orders can lag new government funding announcements by many months. If political constraints or economic slowdowns reduce the pace of actual project execution in 2026, or if the incoming Congressional session introduces uncertainty around tariff policy continuation, order flow could weaken materially from current levels, creating downward pricing pressure.

Global Supply and Trade Tensions

Chinese steelmakers, facing domestic overcapacity and softer demand, have increased export activity at deep discounts (averaging $470 per ton in November 2025). While tariffs shield U.S. mills from direct Chinese competition, they create indirect pressure through deflated global pricing and potential political backlash. Other trade partners, including the European Union, may introduce retaliatory tariffs or trade restrictions that complicate supply chains and create uncertainty. The durability of Nucor’s pricing ultimately depends on the political durability of the tariff regime – a factor beyond management’s control.

The Role of Nearshoring and Long-Term Structural Demand

An underappreciated driver of sustained steel demand is the nearshoring trend – the deliberate relocation of manufacturing capacity from distant locations (particularly China) to locations closer to North American end-customers. Nearshoring is being driven by tariff policy, supply chain resilience concerns following the COVID-19 pandemic, and the desire to reduce logistics costs and lead times. Korean steelmakers Hyundai Steel and Posco have announced investments in a new steel plant in Louisiana, while other foreign steelmakers have increased U.S. capacity investments.

This nearshoring trend provides durable, long-term support for steel demand independent of the business cycle. As manufacturing relocates to North America, it brings with it associated steel consumption for industrial equipment, manufacturing facilities, transportation, and product fabrication. This structural shift in supply chain geography should provide upside support to North American steel demand and pricing for years to come, even if shorter-term demand cycles turn negative.

Conclusion: Nucor’s Pricing Power Reflects Structural Change in the Steel Market

Nucor’s nine-week streak of $10 per ton price increases, bringing HRC pricing to $950 per ton ($1,000 for CSI) in December 2025, represents more than a cyclical uptick in market conditions. Rather, it reflects a fundamental realignment of the North American steel market driven by tariff policy, sustained infrastructure demand, improved producer discipline, and structural shifts in global supply chain geography. The convergence of protective tariffs eliminating import competition, robust construction spending providing demand pull-through, and competitive mills implementing similar pricing all point to conditions that should support elevated steel pricing through at least the next several quarters.

However, steelmakers and their customers must remain vigilant to potential headwinds. Tariff policy, while currently supportive, is inherently political and subject to change. Seasonal demand patterns and inventory buildup cycles could create temporary pricing pressure. Global overcapacity and export competition, particularly from China, create ongoing competitive pressure even if tariffs shield U.S. producers. End-user caution about accumulating expensive inventory could dampen order flow heading into 2026. And broader macroeconomic risks – including potential recession, reduced government spending, or increased financing costs – could undermine the construction and infrastructure demand that has supported current pricing levels.

For steel industry professionals, supply chain managers, and investors, Nucor’s pricing moves should be interpreted as a signal of current market strength and management confidence in durable demand. The company’s willingness to raise prices steadily for nine consecutive weeks, supported by competitive pricing moves from peers, reflects conviction that demand will absorb these increases without significant volume loss. But that confidence should be balanced with recognition that the steel market remains cyclical, tariff policy remains political, and complacency about demand durability or tariff durability could lead to painful corrections if circumstances shift.

The most prudent approach for downstream customers is to maintain balanced inventory positioning – neither speculating excessively on further price increases (which could accelerate if they fail to materialize), nor ignoring the likely persistence of tariff support and infrastructure demand. For investors in Nucor and other steelmakers, the current environment offers attractive near-term earnings potential, but long-term positioning should reflect the reality that tariff benefits could be modified or withdrawn, and cyclical demand patterns remain intact even with structural improvements in the underlying market.

SOURCES

Nucor’s New Pricing Strategy Amid Financial Struggles – https://www.indexbox.io/blog/nucors-new-pricing-strategy-amid-financial-struggles/

June 2025: 50% US Tariffs Steel and Aluminum Impact – BCG – https://www.bcg.com/publications/2025/june-2025-update-impact-us-tariffs-50-percent-on-steel-aluminum

Hot Rolled Coil Industry Report – https://www.imarcgroup.com/hot-rolled-coil-pricing-report

Nucor Cuts Hot Rolled Coil Prices for the First Time in 2025 Amid Market Shifts – https://vietnamsteel.com/blog/news-2/nucor-cuts-hot-rolled-coil-prices-for-the-first-time-in-2025-amid-market-shifts-1356

2025 Steel Tariffs Explained: Everything You Need to Know – Indeavor – https://www.indeavor.com/blog/2025-american-steel-tariffs/

The Global Hot-Rolled Coil (HRC) Market Has Experienced a Stable and Upward Trend – https://steelworldreview.com/en/the-global-hot-rolled-coil-hrc-market-has-experienced-a-stable-and-upward-trend-since-early-nove

Nucor’s Q3 2025 Earnings Guidance: Navigating a Volatile Steel Market – https://www.ainvest.com/news/nucor-q3-2025-earnings-guidance-navigating-volatile-steel-market-strategic-resilience-2509/

Nucor Reports Results for the First Quarter of 2025 (PDF) – https://s202.q4cdn.com/531038915/files/doc_news/Nucor-Reports-Results-for-the-First-Quarter-of-2025-2025.pdf

North American Steel Outlook 2025: Demand to Rise with Automotive Output – Fastmarkets – https://www.fastmarkets.com/insights/north-american-steel-outlook-2025-demand-to-rise-with-automotive-output-2025-preview/

Section 232 Tariffs Impact on Global Trade – Green Worldwide – https://www.greenworldwide.com/section-232-steel-aluminum-tariffs-rise-to-50-as-u-s-expands-reciprocal-duties-to-non-metal-conte

Nucor (NUE) Earnings Date and Reports 2025 – MarketBeat – https://www.marketbeat.com/stocks/NYSE/NUE/earnings/

Steel Industry Trends 2025 – FedSteel – https://www.fedsteel.com/insights/steel-industry-trends-2025/

Section 232 Tariffs on Steel & Aluminum – STR Trade – https://www.strtrade.com/trade-news-resources/tariff-actions-resources/section-232-tariffs-on-steel-aluminum

Nucor (NUE) Q2 2025 Earnings Call Transcript – The Motley Fool – https://www.fool.com/earnings/call-transcripts/2025/08/04/nucor-nue-q2-2025-earnings-call-transcript/

worldsteel Short Range Outlook October 2025 – https://worldsteel.org/media/press-releases/2025/worldsteel-short-range-outlook-october-2025/

Hot Topics in International Trade – December 2025 – Section 232 – JD Supra – https://www.jdsupra.com/legalnews/hot-topics-in-international-trade-3955250/

Nucor Reports Results for the Second Quarter of 2025 – Yahoo Finance – https://finance.yahoo.com/news/nucor-reports-results-second-quarter-203000507.html

2025 Construction Industry Outlook: Costs, Growth & Trends – Buildern – https://buildern.com/resources/blog/construction-industry-outlook/

What the Data Says: Steel Price Updates – Gordian – https://www.gordian.com/resources/steel-price-updates/

Summer 2025 Construction Market Trends – Skanska – https://interactive.usa.skanska.com/skanska/2025-summer-construction-market-trends/p/1

2025 Crude Steel Production Forecast – Fastmarkets – https://www.fastmarkets.com/insights/fastmarkets-2025-crude-steel-production-forecast/

Monthly Construction Spending, August 2025 (PDF) – U.S. Census Bureau – https://www.census.gov/construction/c30/pdf/release.pdf

Steel Market Forecast 2025-2026: Global Price Outlook – https://www.steelonthenet.com/resources/market-data/market-outlook.html

Nucor Continues Series of Price Increases for Hot-Rolled Coil – GMK Center – https://gmk.center/en/news/nucor-continues-series-of-price-increases-for-hot-rolled-coil/

Disclaimer

The content provided in this article is for general informational purposes only and does not constitute financial, legal, or professional advice. Readers should seek consultation with qualified professionals before making any financial, investment, or legal decisions. We disclaim any liability for losses, damages, or adverse outcomes resulting from decisions made based on the information presented herein.

Check out our most recent articles below:

- [New eBook] Steel Buyers Decision Framework

- HRC CSP Climbs Again | Is the Ceiling Coming Near?

- Steel Procurement Framework: Buy, Wait, or Hedge?

- HRC CSP Hits $1,080 | Input Costs Climb | Capacity at 80.4%

- Steel Forecasting 2026: The Old Model Fails, A New Framework

Season’s Greetings from Steel Industry News!

As we wrap up another landmark year in steel, we want to thank our readers, partners, and industry leaders who make innovation and progress possible every day.

📬 Enjoying this article? Do not miss the next one.

Subscribe below to the Steel Industry News email newsletter to get the latest updates delivered straight to your inbox, including comprehensive reporting on the steel industry, plus the latest podcast, video, ebooks, and industry insights, so you receive the most recent steel news reports in one easy-to-read format

Your all-access pass to steel industry insight – now 50% off for the holidays! (Through Jan 1st 2026) – Get The Steel Industry Newsletter’s best annual package for only $300/year – that’s a $300 savings off the regular $600 annual price. You’ll enjoy six months free compared to the monthly plan.

Stay informed and connected as we move into a bright and resilient new year for the industry.

🔗 🔐 Annual Plan: Just $300/year – that’s 6 months free (a 50% discount compared to monthly)

Wishing you strength, success, and prosperity this holiday season and beyond,

The Steel Industry News Team

By subscribing you agree to our Terms of Use, our Privacy Policy and our Information collection notice