Current Nucor CSP Steel Price Reduction

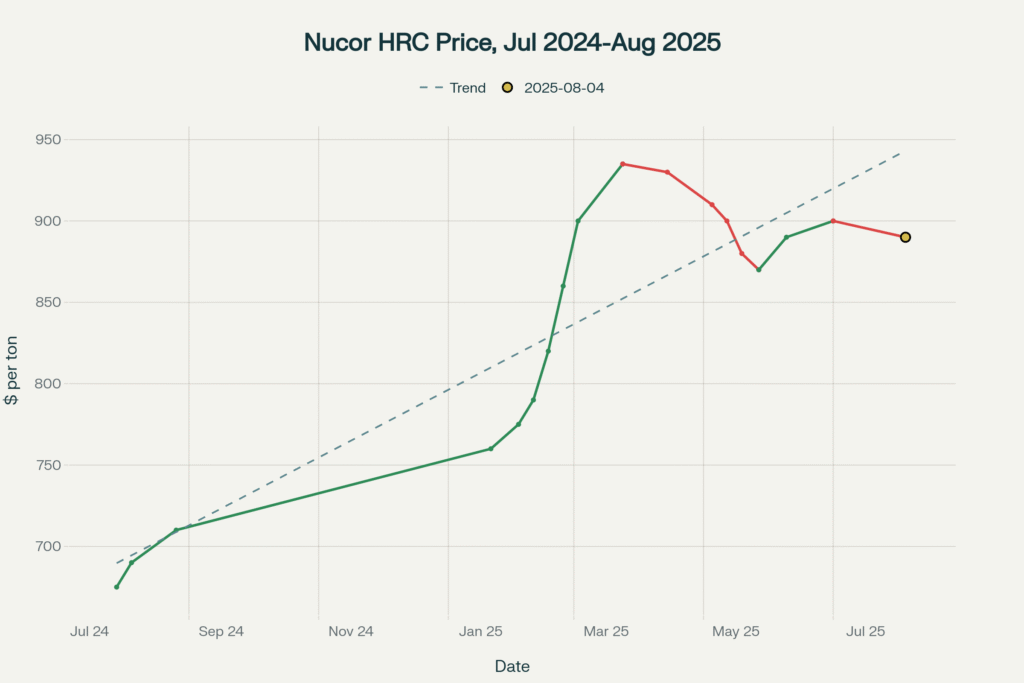

Nucor Corporation has announced another significant price reduction in its Consumer Spot Price (CSP) for hot-rolled coil (HRC) steel, setting the base price at $875 per ton effective August 11, 2025, for all producing mills except California Steel Industries (CSI), where the price stands at $935 per ton. This marks the second consecutive decrease following last week’s reduction to $890 per ton, representing a $15 per ton decline from the previous week and highlighting the ongoing market correction in steel pricing.

The dual pricing structure between Nucor’s standard mills and its California Steel Industries subsidiary continues to reflect regional market dynamics, with CSI maintaining a $60 premium over base pricing due to West Coast market conditions and logistics considerations. This pricing differential has been a consistent feature of Nucor’s strategy, acknowledging the unique supply-demand dynamics in different geographic markets.

Recent Pricing Trajectory and Market Context

The current $875 per ton price represents a significant retreat from the peak of $935 per ton reached in March 2025, marking a 6.4% decline from the year’s high. However, it’s crucial to understand this correction within the broader context of Nucor’s remarkable pricing journey over the past year.

Key Pricing Milestones:

- July 2024: $675/ton baseline price

- March 2025: Peak at $935/ton representing a 38.5% increase

- Current August 2025: $875/ton, still 29.6% above baseline

The recent price holding pattern around $900 per ton during June and July 2025 demonstrated Nucor’s attempt to stabilize pricing at elevated levels. However, market pressures including softening demand, increased inventory levels, and competitive dynamics have forced the company to implement these consecutive reductions.

Comprehensive Market Analysis: Why Nucor is Reducing Prices

Weakening End-User Demand Across Key Sectors

Automotive Industry Challenges

The automotive sector, which represents 20-25% of steel demand, has experienced significant headwinds impacting Nucor’s pricing strategy. U.S. auto production fell 8% year-over-year in Q1 2025, with EV sales growth slowing and inventories rising. This downturn in the largest consumer of HRC has created substantial downward pressure on steel pricing.

Despite long-term optimism about automotive steel demand, with the global automotive steel market projected to reach $112.4 billion by 2033 with a 4.1% CAGR, near-term challenges persist. The shift toward electric vehicles, while creating demand for high-strength steel products, has also introduced uncertainty in traditional steel consumption patterns.

Construction and Infrastructure Slowdown

The construction sector has faced multiple challenges contributing to reduced steel demand. High interest rates and delayed infrastructure spending led to a 10% drop in new project starts. The Housing Market Index dropped to 34 in May 2025, down from 40 in April, marking the lowest level since November 2023. These factors have significantly impacted demand for structural steel products. It is noteworthy that The Dodge Momentum Index (DMI) surged to a record high of 280.4 in July 2025, marking a sharp increase of 20.8% from June’s upwardly revised reading of 232.1. Both the institutional and commercial sectors contributed significantly, with institutional planning up 35.1% and commercial planning up 14.2%. This growth was driven by several major projects, particularly in data centers, research & development labs, hospitals, and service stations, while steady activity continued for hotels, warehouses, and recreation sector projects.

Manufacturing Sector Contraction

Manufacturing conditions have deteriorated, with PMI indices dipping below 50 in April 2025, signaling contraction and softer steel orders. The ISM Manufacturing PMI for July fell to 48%, marking the fifth consecutive month of contraction and the lowest level in ten months. This broad-based manufacturing weakness has reduced industrial demand for steel products.

Inventory and Supply Chain Dynamics

Elevated Service Center Inventories

Service centers and distributors have been running higher-than-normal inventories, with inventory-to-sales ratios hitting 1.48 in April 2025, above the 5-year average of 1.32. This inventory buildup has reduced immediate purchasing pressure and contributed to pricing softness.

Buyer Behavior Changes

Market participants have adopted a “wait-and-see” mentality, with buyers delaying purchases in anticipation of further price drops. This cautious approach has reinforced downward pricing pressure as immediate demand has decreased while supply remains adequate.

Competitive Market Pressures

Import Competition Despite Tariffs

Despite 50% Section 232 tariffs implemented in June 2025, import offers for HRC from Asia and Turkey have increased, with landed prices as low as $845/ton. This persistent import competition has limited domestic mills’ pricing power, even with substantial tariff protection.

Domestic Competitor Strategies

Cleveland-Cliffs has maintained more aggressive pricing, with its July order book at $950/ton, creating a significant spread with Nucor’s pricing. Cliff’s most recent price announcement was on June 16, with no additional monthly updates since, diverging from their previously scheduled pricing communications.

Input Cost Considerations

Scrap Steel Price Movements

Scrap steel prices, a primary input for Nucor’s electric arc furnaces, declined $20/ton in April and another $30/ton in May. This input cost relief has provided some margin cushion, allowing Nucor to reduce prices while maintaining profitability.

However, graphite electrode costs rose 14% due to supply chain disruptions, partially offsetting scrap savings. The net effect of input cost changes has still been favorable for EAF producers like Nucor.

Tariff Impact and Trade Policy Effects

Section 232 Tariff Escalation

The Trump administration’s decision to double Section 232 tariffs from 25% to 50% on June 4, 2025, was expected to provide significant support for domestic steel prices. However, the initial market reaction has been more muted than anticipated, with domestic prices continuing to face pressure despite the substantial tariff increase.

Market Response to Tariffs:

- Import offers have adjusted upward but remain competitive

- Domestic mills initially paused quoting to assess market conditions

- The tariff impact has been partially offset by continued weak domestic demand

Economic Uncertainty and Policy Implications

The persistent uncertainty surrounding trade policies has contributed to reduced industrial investment and delayed purchasing decisions. While tariffs provide protection against imports, they cannot address fundamental demand weakness in key end-use sectors.

Regional and Global Steel Market Context

Capacity Utilization Trends

U.S. steel capacity utilization has remained below optimal levels, with recent data showing rates around 74-79%. This is below the 80% threshold typically considered necessary for industry viability and profitability. The ongoing capacity underutilization reflects the broader demand challenges facing the industry.

Global Steel Market Pressures

International Overcapacity

Global steel capacity utilization has fallen below 75% in early 2025, compared to 77.3% in Q4 2024, indicating persistent oversupply conditions. This global overcapacity continues to pressure international steel prices and indirectly affects U.S. domestic pricing through import competition.

European Market Challenges

The European steel market faces similar challenges, with apparent steel consumption expected to decline 0.9% in 2025. EU steel-using sectors experienced output contraction of 3.7% in 2024, with another recession anticipated in 2025. These international headwinds contribute to global pricing pressure.

Strategic Implications for Market Participants

For Steel Buyers and End Users

The current pricing environment presents strategic opportunities for steel buyers:

- Favorable procurement timing with prices retreating from peak levels

- Improved negotiating position as mills seek to maintain volume

- Inventory optimization opportunities with more predictable pricing trends

However, buyers should note that current prices remain significantly elevated compared to historical baselines, with cumulative increases of nearly 30% since July 2024.

For Steel Producers and Competitors

Nucor’s Strategic Position

Nucor’s pricing strategy demonstrates a pragmatic approach, prioritizing volume and customer relationships over short-term price maximization. The company’s flexibility as an EAF producer allows for more responsive pricing compared to integrated competitors.

Competitive Dynamics

The pricing spread between Nucor and Cleveland-Cliffs creates interesting market dynamics, with buyers evaluating price advantages against lead times and service levels. This competitive positioning may intensify if market conditions continue to weaken.

Future Market Outlook and Price Projections

Near-Term Price Expectations

Market participants expect continued pricing volatility through the remainder of 2025. The $875/ton CSP price may establish a new reference point, though further adjustments remain possible depending on:

- Demand recovery in key end-use sectors

- Import price movements despite tariff protection

- Raw material cost trends, particularly scrap steel pricing

- Inventory adjustment cycles at service centers and distributors

Medium-Term Industry Fundamentals

Demand Recovery Scenarios

Recovery prospects remain conditional on broader economic improvements:

- Automotive sector stabilization and EV transition progress

- Infrastructure spending implementation and housing market recovery

- Manufacturing sentiment improvement and industrial investment resumption

Supply-Side Considerations

New capacity additions and industry investments in green steel technologies may reshape long-term supply dynamics. However, these developments are primarily medium to long-term considerations rather than immediate pricing factors.

Conclusion: Navigating the Current Steel Market Environment

Nucor’s latest price reduction to $875 per ton reflects the complex interplay of weakened demand, elevated inventories, and competitive pressures that characterize the current steel market environment. The second consecutive decrease signals that the industry’s attempt to maintain pricing around $900 per ton has proven unsustainable given current market conditions.

While the 50% tariff increase provides import protection, it cannot address fundamental domestic demand weakness across key sectors including automotive, construction, and manufacturing. The ongoing pricing volatility underscores the challenges facing steel producers as they balance volume maintenance with margin preservation.

Market participants should prepare for continued uncertainty in steel pricing, with potential for both further corrections and eventual recovery depending on broader economic conditions and end-use demand patterns. The current environment demands flexible procurement strategies and careful attention to inventory management as the market seeks new equilibrium pricing levels.

The $875 per ton price point may represent a more sustainable level given current market fundamentals, though continued monitoring of demand indicators, inventory levels, and competitive dynamics will be essential for understanding future price movements in this evolving market landscape.

Disclaimer: This article is intended for informational purposes only and does not constitute financial, investment, or trading advice. Readers should consult a qualified financial professional before making any financial decisions.

SOURCES

Nucor Cuts CSP Steel Price: Price History & Market Analysis

https://steelindustry.news/nucor-cuts-csp-steel-price-price-history-market-analysis/

Nucor Announces CSP Price Cut: Market Analysis, Price History & What’s Next

https://steelindustry.news/nucors-nucor-announces-csp-price-cut-market-analysis-price-history-and-whats-next/

Nucor cuts prices for hot rolled coils by $20/t – GMK Center

https://gmk.center/en/news/nucor-cuts-prices-for-hot-rolled-coils-by-20-t/

Nucor lowers HRC CSP to $930/ton – Steel Market Update

https://www.steelmarketupdate.com/2025/04/14/nucor-lowers-hrc-csp-to-930-ton/

US Steel Prices & Pricing of Steel: Latest Market Intelligence | Ryerson

https://www.ryerson.com/metal-resources/metal-market-intelligence/are-steel-prices-coming-down

Nucor Introduces New Hot-Rolled Coil Spot Pricing (Investor Release)

https://investors.nucor.com/news/news-details/2024/Nucor-Introduces-New-Hot-Rolled-Coil-Spot-Pricing/default.aspx

Nucor lowers HRC price to $910/ton – Steel Market Update

https://www.steelmarketupdate.com/2025/05/05/nucor-lowers-hrc-price-to-910-ton/

Nucor raises HRC spot price by $10/st to $760 | Latest Market News – Argus Media

https://www.argusmedia.com/en/news-and-insights/latest-market-news/2651596-nucor-raises-hrc-spot-price-by-10-st-to-760

Nucor Reports Results for the Second Quarter of 2025 (Company Report)

https://nucor.com/news-release/nucor-reports-results-for-the-second-quarter-of-2025-122976

Check out our most recent articles below:

- Why Most U.S. Manufacturers Still Are Not Using AI at Scale

- HRC CSP Climbs $10 As Global Cost Pressure Stacks Against Cautious Demand

- Tariff Update May 2026: Section 232 Restructured, IEEPA Struck Down

- CSP HRC Hits $1,095 as Construction Bends

- [New eBook] Steel Buyers Decision Framework

📬 Enjoying this article? Do not miss the next one.

SUBSCRIBE below to the Steel Industry News email newsletter to get the latest updates delivered straight to your inbox. Includes a comprehensive reporting of all key topics impacting the steel industry. 🌍The Most Recent Steel News Reports — in one easy-to-read weekly format

🔐 Annual Plan: Just $300/year – that’s 6 months free . – 💰 Best value of unbiased, timely reporting in the industry.

By subscribing you agree to our Terms of Use, our Privacy Policy and our Information collection notice