Introduction

The landscape of American trade policy underwent a dramatic transformation with the resurgence and expansion of steel tariffs under Section 232 of the Trade Expansion Act of 1962. What began as a national security measure in 2018 has evolved into one of the most comprehensive and controversial trade interventions in modern U.S. history. On August 18, 2025, the scope of these tariffs expanded dramatically when the Commerce Department added 407 new product categories to the list of steel and aluminum derivatives subject to a crushing 50% tariff rate.

The recent expansion represents a watershed moment in American trade policy, extending tariffs beyond raw steel and aluminum to encompass everything from wind turbines and mobile cranes to seemingly unrelated products like milk packaging and shampoo containers. This comprehensive approach reflects the Trump administration’s determination to address what it views as fundamental threats to America’s industrial base and national security.

The implications of this policy shift extend far beyond the steel industry itself. With downstream industries employing roughly 50 times more workers than steel production, the economic ripple effects touch virtually every sector of the American economy. From automotive manufacturing to construction, from food packaging to energy infrastructure, the expanded tariffs are reshaping supply chains, altering competitive dynamics, and forcing businesses to navigate an increasingly complex trade environment.

Understanding Section 232: Legal Foundation and Authority

Historical Context and Legislative Framework

Section 232 of the Trade Expansion Act of 1962 grants the President extraordinary authority to impose trade restrictions when imports threaten national security. Originally signed into law by President John F. Kennedy, who called it “the most important piece of legislation affecting economies since the passage of the Marshall Plan,” the statute provides sweeping discretionary power to the executive branch.

The legal framework requires the Secretary of Commerce to investigate whether imports are “being imported into the United States in such quantities or under such circumstances as to threaten to impair the national security”. This investigation process, which must be completed within 270 days, examines domestic production capacity, national defense implications, employment impacts, and other considerations relevant to national security.

Between 1962 and 2020, Commerce initiated only 31 Section 232 investigations, with the President acting on just nine occasions. The last time a president imposed tariffs under Section 232 before the Trump administration was in 1986, making the recent activation of this authority particularly significant.

The Trump Administration’s Invocation

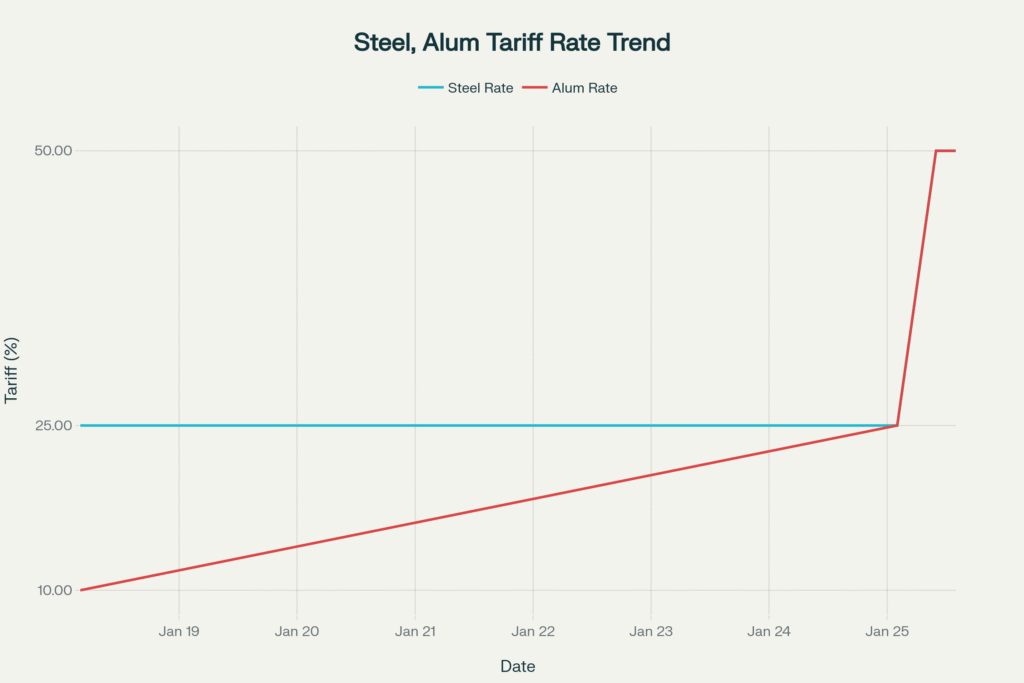

President Trump’s March 2018 invocation of Section 232 marked a dramatic departure from historical precedent. The Commerce Department’s investigation, led by then-Secretary Wilbur Ross, determined that steel and aluminum imports were undermining the domestic industry’s ability to meet national security production requirements. This finding provided the legal foundation for imposing a 25% tariff on steel imports and a 10% tariff on aluminum imports.

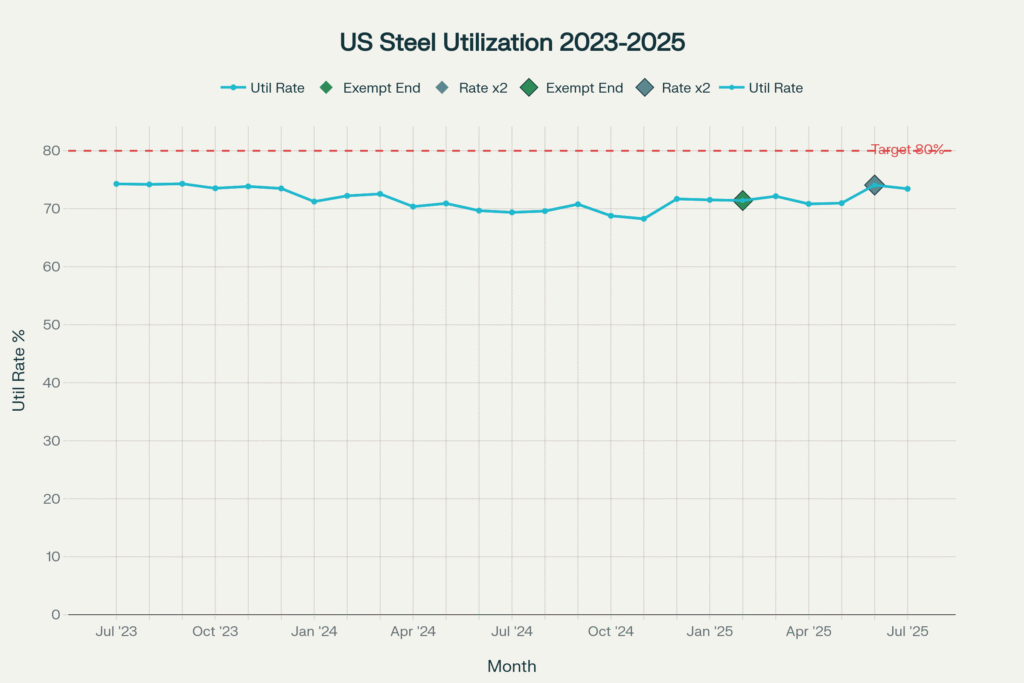

The national security rationale centered on several key arguments: the closure of domestic steel and aluminum plants, reduced capacity utilization rates below the targeted 80% threshold, and concerns about supply chain vulnerabilities in critical defense applications. The administration argued that a robust domestic steel and aluminum industry was essential for military readiness and economic resilience.

Legal Challenges and Judicial Response

The Section 232 tariffs faced numerous legal challenges, but courts have consistently upheld the President’s authority. In USP Holdings, Inc. v. United States, the Court of International Trade affirmed that the tariffs did not violate constitutional separation of powers principles. The Supreme Court declined to hear appeals challenging the tariffs, effectively ending major constitutional challenges.

However, courts have imposed some limitations. In Transpacific Steel LLC v. United States, the Court of International Trade ruled that President Trump violated statutory timing constraints when he doubled tariffs on Turkish steel imports outside the prescribed 90-day window. This decision highlighted that while Section 232 grants broad authority, it does not provide unlimited presidential discretion.

US Steel Industry Capacity Utilization Rates (2023-2025) showing the impact of tariff policy changes on domestic steel production efficiency

The Evolution of Steel Tariff Policy (2018-2025)

Initial Implementation and Early Modifications

The original 2018 tariffs applied broadly but included significant exemptions and alternative arrangements for key allies. Countries including Canada, Mexico, the European Union, Japan, South Korea, Argentina, Australia, Brazil, and the United Kingdom received various forms of relief through quotas, exemptions, or reduced rates.

These exemptions, while diplomatically expedient, created what the Trump administration later characterized as “loopholes” that undermined the tariffs’ effectiveness. The administration argued that China and other countries with excess capacity exploited these exemptions to circumvent the tariffs through transshipment and other avoidance mechanisms.

The February 2025 Reset

On February 10, 2025, President Trump issued Proclamations 10895 and 10896, fundamentally restructuring the tariff regime. These proclamations eliminated all country-specific exemptions and alternative arrangements, creating a uniform 25% tariff on steel and aluminum imports from all countries. The reset also introduced strict “melted and poured” requirements for steel and “smelted and cast” requirements for aluminum to qualify for duty-free treatment.

The June 2025 Escalation

The most dramatic escalation came on June 3, 2025, when President Trump issued a proclamation doubling the tariff rates to 50% for both steel and aluminum. This increase applied to all countries except the United Kingdom, which remained at 25% while continuing trade negotiations under the U.S.-UK Economic Prosperity Deal.

The decision to double tariffs reflected the administration’s assessment that the previous 25% rate was insufficient to achieve the program’s objectives. Commerce Department monitoring indicated that capacity utilization rates remained below the targeted 80% threshold, and foreign competition continued to pressure domestic producers.

August 2025: The Derivative Products Expansion

The August 2025 expansion represents the most comprehensive extension of Section 232 authority to date. The Commerce Department’s addition of 407 new Harmonized Tariff Schedule codes extends the 50% tariff to a vast array of products containing steel and aluminum components.

The expanded list includes major industrial equipment such as wind turbines, mobile cranes, bulldozers, and railcars, as well as consumer products like furniture, appliances, and even food packaging. Notably, the tariffs apply only to the steel and aluminum content of these products, with non-metallic components subject to other applicable tariffs.

Evolution of US Steel and Aluminum Tariff Rates (2018-2025) showing the escalation from initial Section 232 levels to current 50% rates

Economic Impact Analysis: Winners and Losers

Steel Industry Performance and Benefits

The steel industry has experienced measurable benefits from the tariff protection. According to the American Iron and Steel Institute, the industry added approximately 1,000 jobs between March 2018 and November 2019. Recent data shows that U.S. steel production capacity utilization reached 79.5% in the week ending August 9, 2025, approaching the administration’s 80% target.

Year-to-date steel production through August 16, 2025, totaled 55.92 million net tons, representing a 1.3% increase from the same period in 2024. This production increase occurred despite overall global steel output declining by 4.7% in 2024, suggesting that the tariffs successfully diverted demand to domestic producers.

Steel companies have responded positively to the enhanced protection. Major producers including Nucor, Cleveland-Cliffs, and U.S. Steel saw significant stock price gains following tariff announcements. The industry has also announced substantial capital investments, with more than $10 billion committed to new mills since the original tariffs were implemented.

Devastating Impact on Downstream Manufacturing

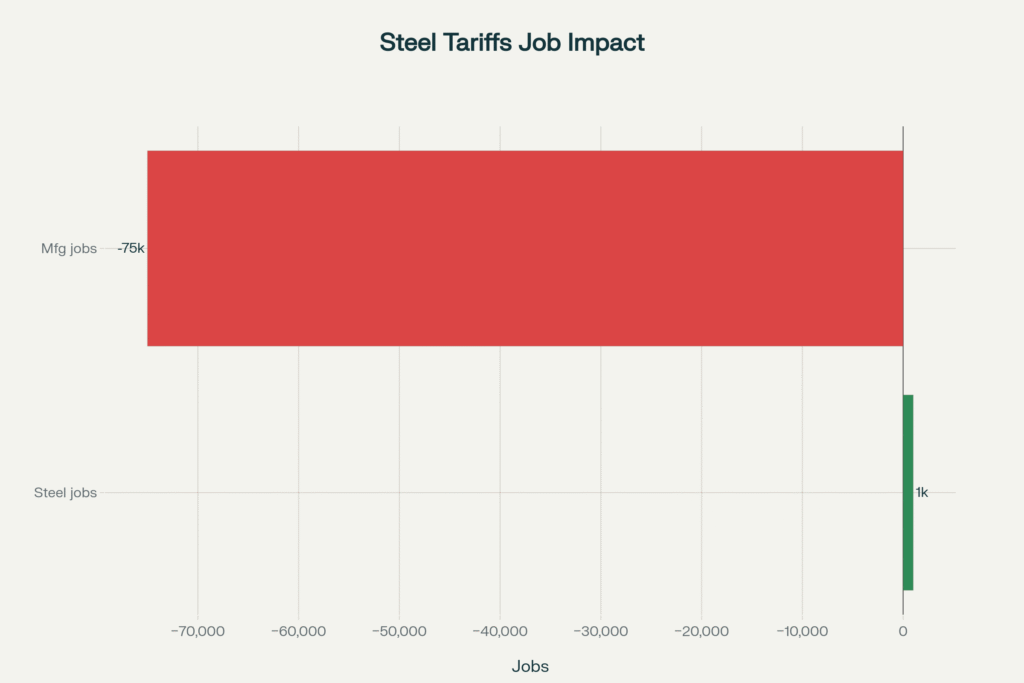

While the steel industry celebrated, the broader manufacturing sector faced severe headwinds. A comprehensive Federal Reserve study found that increased input costs from steel and aluminum tariffs resulted in approximately 75,000 fewer manufacturing jobs by mid-2019. This represents a job loss ratio of roughly 75:1 compared to steel industry gains.

The impact extends across numerous sectors that rely on steel and aluminum as inputs. Downstream industries employ approximately 12 million Americans, with nearly 2 million working in steel-intensive industries where steel inputs comprise at least 5% of total requirements. For aluminum, the employment ratio is even more stark, with 177 downstream workers for every aluminum production job.

Manufacturing companies face multiple challenges from higher steel costs. Caterpillar, the world’s largest construction equipment manufacturer, increased prices by over $100 million to offset higher steel costs during the first round of tariffs. Similarly, automotive manufacturers face additional costs of approximately $2,000 per vehicle due to the steel content of cars.

Price Inflation and Consumer Impact

The tariffs have contributed significantly to domestic price inflation for steel and aluminum products. U.S. steel benchmarks now trade at roughly twice world prices, with hot-rolled coil averaging around $900 per ton compared to $450 per ton for world export prices. Aluminum prices have increased even more dramatically, rising 65% year-to-date through 2025.

According to recent Consumer Price Index data, goods prices have increased substantially in tariff-affected categories. Used vehicle prices rose 4.8% over the previous year, while furniture and home goods saw increases of 11-20% as manufacturers passed through higher steel costs. Food packaging costs have also risen as aluminum can manufacturers face higher input costs.

Economists estimate that the cumulative impact of all 2025 tariffs raises consumer prices by approximately 2.3%, equivalent to a loss of purchasing power of $3,800 per household in 2024 dollars. This represents a significant regressive tax that disproportionately affects lower-income households.

Steel Tariffs Employment Impact: 1,000 steel jobs gained vs 75,000 manufacturing jobs lost, showing the net negative effect on US employment

Industry-Specific Impacts and Case Studies

Automotive Sector: Steel’s Biggest Consumer

The automotive industry represents one of the largest consumers of steel, using approximately half a ton of steel per vehicle. With the tariff rate at 50%, automakers face potential cost increases of over $2,000 per vehicle for steel content alone. Major manufacturers including Ford, General Motors, and Tesla have indicated they may need to pass these costs to consumers through higher vehicle prices.

The impact extends beyond finished vehicles to the vast automotive supply chain. Auto parts manufacturers, which employ hundreds of thousands of Americans, face a double squeeze: higher input costs from steel tariffs and potential loss of export markets due to retaliatory measures. The industry’s just-in-time manufacturing model makes it particularly vulnerable to supply chain disruptions caused by rapid tariff changes.

Construction Industry: Building Costs Soar

The construction sector faces significant challenges as steel represents a critical input for everything from residential housing to major infrastructure projects. Industry leaders report frequent reassessment of project timelines and budgets to adapt to fluctuating steel costs. The lack of advance notice for the August 2025 expansion created particular difficulties for projects already under contract.

Home builders face a particularly acute challenge, as steel framing, rebar, and other components directly affect housing affordability. With the U.S. facing a housing shortage, higher construction costs from steel tariffs exacerbate affordability challenges for American families. Commercial construction projects have also experienced budget overruns and delays as contractors struggle to manage volatile steel costs.

Food and Beverage Packaging: Hidden Consumer Impact

One of the most surprising aspects of the August 2025 expansion was the inclusion of products like food packaging, which affects everyday consumer goods. Aluminum cans used for beverages, soups, and other food products now face 50% tariffs on their aluminum content. The Can Manufacturers Institute estimates these costs will inevitably be passed to food processors and ultimately consumers.

Robert Budway, former president of the Can Manufacturers Institute, explains the cost pass-through mechanism: “For can makers, we pass the costs of the tariff onto our customers who are the food processors, and then they pass the cost on to the consumer eventually”. This creates a hidden tax on basic consumer goods that many Americans may not directly associate with trade policy.

Energy Sector: Infrastructure Implications

The energy sector faces substantial challenges from steel tariffs, particularly as the U.S. seeks to modernize its electrical grid and expand renewable energy capacity. Wind turbines, which were specifically included in the August 2025 expansion, rely heavily on steel for towers and other components. This creates a contradiction with clean energy goals, as higher costs for renewable energy infrastructure may slow the transition away from fossil fuels.

Oil and gas infrastructure also depends heavily on steel for pipelines, drilling equipment, and refineries. The Energy Information Administration estimates that higher steel costs could add billions to infrastructure projects, potentially slowing energy development and increasing consumer energy costs.

Global Trade Dynamics and International Response

Chinese Steel Overcapacity:

The fundamental driver behind U.S. steel tariffs is China’s massive steel overcapacity and export surge. China produces over 1 billion tons of steel annually, giving it nearly 10 times the steelmaking capacity of the United States. In 2024, China exported a record 110.72 million tons of steel, up from 94.5 million tons in 2023.

This export surge has created a large amount of cheap Chinese steel onto global markets. Chinese steelmakers, facing weak domestic demand due to a slowing construction sector, have increasingly turned to exports to maintain production levels. The European steel industry reports that Chinese exports to key markets rose by 98% in 2023, with spillover effects reaching EU markets.

However, recent analysis suggests this trend may be peaking. Goldman Sachs projects that Chinese steel exports will decline by 3% in 2025 and up to one-third in 2026 as domestic production falls and trade barriers increase worldwide. Rising anti-dumping investigations globally are making it increasingly difficult for Chinese producers to access international markets.

International Retaliation and Trade Wars

The expansion of U.S. steel tariffs has triggered significant retaliatory measures from trading partners. Canada, the largest supplier of steel to the United States, has imposed retaliatory duties on approximately $20 billion of U.S. exports including tools, computers, sports equipment, and other products. The European Union has announced retaliation targeting $28 billion of U.S. exports including beef, poultry, motorcycles, bourbon, and jeans.

The retaliation creates a vicious cycle that harms U.S. exporters. During the first Trump administration, U.S. spirits exports to Europe slumped by approximately 40% after the EU imposed retaliatory duties. The spirits industry, which employs about 1.7 million American workers, illustrates how tariff retaliation can devastate export-dependent sectors.

Brazil has formally challenged U.S. trade investigations at the WTO, questioning the validity of Section 232 national security claims. Other countries are exploring similar challenges, though the effectiveness of WTO dispute resolution remains limited due to U.S. actions that have paralyzed the appellate process.

World Trade Organization Challenges

The WTO has ruled that U.S. Section 232 steel and aluminum tariffs violate international trade rules and should be removed. A WTO dispute resolution panel determined that the national security justification was improper and didn’t merit the security exception under WTO rules.

However, the ruling has had limited practical impact. The Biden administration rejected the WTO decision, and the Trump administration has maintained the same position. Assistant U.S. Trade Representative Adam Hodge stated that “issues of national security cannot be reviewed in WTO dispute settlement and the WTO has no authority to second-guess the ability of a WTO Member to respond to threats to its security”.

The U.S. has effectively neutralized WTO enforcement by paralyzing the appellate body, making it impossible for other countries to pursue appeals of panel decisions. This has led to calls for fundamental WTO reform, though major economies appear reluctant to engage in multilateral negotiations given current geopolitical tensions.

The Exclusion Process: Bureaucratic Complexity and Industry Influence

Historical Exclusion Statistics

The Commerce Department established an exclusion process to provide relief for companies unable to source steel and aluminum domestically. Between 2018 and 2021, the department received 288,021 exclusion requests—260,450 for steel and 27,571 for aluminum. Of these, 170,084 were granted, 59,134 were denied, and 44,325 were rejected or withdrawn.

The exclusion process revealed the complex dynamics between domestic producers and downstream users. U.S. steel and aluminum producers filed objections against 6,371 steel exclusion requests, and none of the objected requests were approved. This pattern demonstrates the significant influence domestic producers wielded in the exclusion process.

The End of Exclusions

On February 10, 2025, the Trump administration terminated the exclusion process entirely, declaring that all existing exclusions would expire by March 12, 2025. This decision eliminated a critical relief valve that had allowed some companies to manage the economic impact of tariffs. The administration justified this action by arguing that exclusions had created loopholes that undermined the tariffs’ effectiveness.

The termination of exclusions has forced companies to either pay the full 50% tariff rate or find domestic suppliers. For many specialized steel and aluminum products not produced in sufficient quantities domestically, this creates an impossible choice between paying prohibitive tariffs or shutting down operations.

Industry Influence in the Derivative Process

The August 2025 expansion resulted from a formal request process where domestic interested parties could petition Commerce to include additional products. The U.S. Chassis Manufacturers Coalition, American Trailer Manufacturers Coalition, and other industry groups successfully lobbied for inclusion of their competitive products.

Commerce approved nearly all inclusion requests while appearing to ignore objections from downstream users. Legal analysts note that Commerce’s decision memoranda “do not mention any of the objections received, nor do they provide any analysis for why Commerce approved the inclusion over the objections received”. This procedural approach has made the decisions vulnerable to potential court challenges.

Policy Implications and Future Considerations

National Security vs. Economic Efficiency

The steel tariff debate reflects a fundamental tension between national security considerations and economic efficiency. Proponents argue that maintaining domestic steel and aluminum production capacity is essential for military preparedness and economic resilience. The COVID-19 pandemic and recent supply chain disruptions have reinforced concerns about over-reliance on foreign suppliers for critical materials.

However, critics contend that the economic costs far outweigh the security benefits. The Peterson Institute for International Economics estimates that Trump’s steel tariffs cost taxpayers more than $900,000 annually for every job saved or created. This suggests that alternative approaches, such as direct subsidies or strategic stockpiling, might achieve national security objectives more efficiently.

Long-term Competitiveness Concerns

The tariff policy raises serious questions about long-term competitiveness. Rather than investing in automation and efficiency improvements, U.S. steel producers have relied on tariff protection to maintain market share. Data shows that U.S. steel output per hour has fallen 32% since 2017, while overall productivity has increased 15%.

International competitors continue to invest in advanced production technologies, potentially widening the efficiency gap over time. The challenge for policymakers is designing interventions that support domestic industry without creating perverse incentives.

Climate and Environmental Considerations

The global steel industry accounts for approximately 7-11% of global CO₂ emissions, making climate considerations central to trade policy. The European steel industry notes that while EU producers invest in low-carbon production technologies, 60 million tons of new coal-based steel capacity will come online globally by 2026.

U.S. tariffs may inadvertently support higher-emission production by protecting less efficient domestic facilities. A more targeted approach might focus on carbon content rather than country of origin, incentivizing cleaner production regardless of location. This could align trade policy with climate objectives while maintaining competitive pressure for efficiency improvements.

Industry Perspectives

Economic Research Findings

Multiple academic studies have examined the economic impact of steel tariffs with remarkably consistent findings. Research by economists at Harvard, UC Davis, Columbia, the Federal Reserve Bank of New York, and Princeton University all conclude that job losses in downstream industries significantly exceed gains in steel production.

The Federal Reserve Board study by Aaron Flaaen and Justin Pierce provides the most comprehensive analysis, finding that tariffs reduced manufacturing employment by 0.6% by mid-2019. This research methodology controlled for other economic factors, providing strong evidence that the employment effects are directly attributable to tariff policy rather than broader economic trends.

Industry Leader Perspectives

Industry leaders offer sharply divergent views on tariff policy. Kevin Dempsey, president and CEO of the American Iron and Steel Institute, argues that higher tariffs help U.S. steelmakers compete against Chinese dumping and could stimulate investment and job creation. The steel industry views the tariffs as essential for survival against unfair foreign competition.

Conversely, downstream industry representatives express grave concerns about competitiveness. Timothy Zimmerman, CEO of Mitchell Metal Products, describes the impact of previous tariffs: “We saw steel prices rise within a few months about 70% over what they had been… Our suppliers simply broke contracts and gave us an option: Take this or take nothing”. His company lost business to European rivals who didn’t face similar input cost increases.

Academic and Policy Expert Views

Trade economists generally oppose the steel tariffs on efficiency grounds. Katheryn Russ of UC Davis, who has extensively studied tariff impacts, explains: “When there’s a tariff on steel, that can drive up the cost for producers who use steel as an input to make other stuff. And that can prompt them to pull back on hiring”.

However, some experts acknowledge legitimate national security concerns. The challenge, according to policy analysts, is designing targeted interventions that address security vulnerabilities without creating broader economic distortions. This might involve strategic stockpiling, defense production incentives, or targeted subsidies rather than broad-based tariffs.

Conclusion: Balancing Security and Prosperity in Trade Policy

The evolution of steel tariffs from a targeted trade remedy to a comprehensive industrial policy tool represents one of the most significant shifts in U.S. trade policy in decades. The August 2025 expansion to 407 derivative products marks a watershed moment that extends government intervention deep into supply chains across the American economy.

The policy has achieved some of its stated objectives. U.S. steel production has increased, capacity utilization has improved toward the 80% target, and the domestic industry has gained important breathing room against foreign competition. The 50% tariff rate creates substantial protection that has encouraged investment and preserved jobs in steel production.

However, the broader economic evidence suggests that these gains come at enormous cost to the rest of the manufacturing sector and American consumers. The 75,000 manufacturing jobs lost due to higher input costs far exceed the 1,000 steel jobs gained, creating a net negative employment impact. Consumer price increases of $3,800 per household represent a significant regressive tax that hits working families hardest.

The international ramifications are equally concerning. Retaliatory tariffs have cost American exporters billions in lost sales, while WTO challenges and diplomatic tensions strain relationships with key allies. The “America First” approach risks isolating the United States from global supply chains and innovation networks that drive long-term competitiveness.

Moving forward, policymakers face difficult choices about how to balance legitimate national security concerns with economic efficiency and consumer welfare. The steel industry’s struggles reflect real challenges from Chinese overcapacity and unfair trade practices that demand attention. However, the current approach of escalating tariffs appears to create more problems than it solves.

A more sophisticated policy framework might focus on targeted interventions that address specific security vulnerabilities without disrupting entire supply chains. This could include strategic stockpiling of critical materials, defense production incentives for essential industries, or coordinated international action against unfair trade practices. Climate considerations also suggest that carbon content, rather than country of origin, might provide a more effective basis for trade policy in the 21st century.

The steel tariff experience offers important lessons about the complexity of modern trade policy and the unintended consequences of well-intentioned interventions. As global supply chains become increasingly integrated and economic competition intensifies, the challenge for American policymakers is crafting approaches that enhance both security and prosperity rather than trading one for the other.

How will American manufacturing adapt to this new trade policy, and what lessons will guide future interventions in an increasingly complex global economy?

SOURCES

U.S. Department of Commerce. “Adoption and Procedures of the Section 232 Steel and Aluminum Tariff Inclusions Process.”

https://www.federalregister.gov/documents/2025/08/19/2025-15819/adoption-and-procedures-of-the-section-232-steel-and-aluminum-tariff-inclusions-process

Reuters. “US Commerce Dept. widens products subject to steel, aluminum tariffs.” (Aug 15, 2025)

https://www.reuters.com/business/us-commerce-dept-widens-products-subject-steel-aluminum-tariffs-2025-08-15/

White House. “Adjusting Imports of Aluminum and Steel into the United States.” (June 3, 2025)

https://www.whitehouse.gov/presidential-actions/2025/06/adjusting-imports-of-aluminum-and-steel-into-the-united-states/

American Iron and Steel Institute. “Industry Data.” (2025)

https://www.steel.org/industry-data/

Federal Register Notices and Commerce Department Press Releases regarding the August 2025 tariff expansion (multiple Commerce.gov press releases as referenced)

Examples:

https://www.bis.gov/press-release/department-commerce-adds-407-product-categories-steel-aluminum-tariffs

https://www.wiley.law/pressrelease-Commerce-Department-Expands-Section-232-Steel-Derivative-Tariffs-to-Include-Container-Chassis-Imports

Federal Reserve Board, Studies on Steel Tariffs and Employment Impact, including Aaron Flaaen and Justin Pierce research papers (2025)

https://econofact.org/steel-tariffs-and-u-s-jobs-revisited

Investopedia. “Section 232 of the Trade Expansion Act: What It Is and How It Works.” (2025)

https://www.investopedia.com/terms/s/section-232-trade-expansion-act.asp

New York Times. “How Higher Tariffs on Steel and Aluminum Will Affect Companies.” (June 2025)

https://www.nytimes.com/2025/06/04/business/economy/trump-tariffs-steel-aluminum-companies.html

World Trade Organization and related rulings on U.S. Section 232 tariffs and international dispute responses

https://www.aist.org/wto-rejects-section-232-steel-and-aluminum-tariffs

https://www.msci.org/what-the-wto-ruling-against-u-s-section-232-tariffs-means

The Conference Board. “Section 232 Tariff Investigations and Public Comments.” (2025)

https://www.conference-board.org/research/ced-policy-backgrounders/section-232-tariff-investigations-and-public-comments

Yale Budget Lab. “The Fiscal, Economic, and Distributional Effects of All U.S. Tariffs Enacted 2025 through April.” (2024)

https://budgetlab.yale.edu/research/where-we-stand-fiscal-economic-and-distributional-effects-all-us-tariffs-enacted-2025-through-april

Trade Compliance Resource Hub. “Trump 2.0 Tariff Tracker.” (2025)

https://www.tradecomplianceresourcehub.com/2025/08/15/trump-2-0-tariff-tracker/

NPR. “Steel and aluminum tariffs double today, likely pushing prices higher.” (June 2025)

https://www.npr.org/2025/06/04/nx-s1-5422248/trump-steel-aluminum-50-tariffs-double-prices

Peterson Institute for International Economics. Various economic analyses on tariffs and job impacts.

Can Manufacturers Institute and related industry statements on food packaging tariffs (2025).

U.S. Census and YCharts data on capacity utilization and steel production (2025).

Various court rulings and legal analyses on Section 232 tariff challenges, including cases cited: Transpacific Steel LLC v. US, and Supreme Court decisions.

https://www.msci.org/u-s-supreme-court-refuses-to-hear-section-232-tariff-case

https://www.cov.com/en/news-and-insights/insights/2019/03/section-232-tariffs-survive-constitutional-challenge-but-reforms-remain-possible

European Steel Association (Eurofer). Reports on global steel overcapacity and carbon emission challenges (2025).

Associated industry news and market analyses such as American Workforce Group and HBK CPA on sectoral impacts of tariffs (2025).

Check out our most recent articles below:

- Tariff Update May 2026: Section 232 Restructured, IEEPA Struck Down

- CSP HRC Hits $1,095 as Construction Bends

- [New eBook] Steel Buyers Decision Framework

- HRC CSP Climbs Again | Is the Ceiling Coming Near?

- Steel Procurement Framework: Buy, Wait, or Hedge?

📬 Enjoying this article? Do not miss the next one.

SUBSCRIBE below to the Steel Industry News email newsletter to get the latest updates delivered straight to your inbox. Includes a comprehensive reporting of all key topics impacting the steel industry. 🌍The Most Recent Steel News Reports — in one easy-to-read weekly format

🔐 Annual Plan: Just $300/year – that’s 6 months free . – 💰 Best value of unbiased, timely reporting in the industry.

By subscribing you agree to our Terms of Use, our Privacy Policy and our Information collection notice